Stride (LRN), Lone Star Online Academy's Closure, and the Return of Efficacy Risk

Will Lone Star’s recently announced closure force investors to care about virtual school efficacy once again?

First, a bit of housekeeping.

Moving forward, this Substack is going to broaden beyond education. I’ll still write about edtech, but I also expect to write more about defense, energy, and other sectors where I’ve spent a meaningful amount of time doing consulting and investment work.

That’s why I recently renamed the Substack to The Mission Critical Investor rather than the AI Education Investor. I’ll be covering mission critical sectors that are essential for our survival.

Also, I previously promised readers of this Substack to stop writing about the virtual school space and its participants. This follows several pieces I wrote about how large the virtual school market could get and what happens when Stride customers leave. The virtual school market is incredibly interesting given the intersection of business, public policy, academic outcomes, post-pandemic behaviors, and consumer marketing. Fortunately/unfortunately, I noticed that Stride and Pearson employees started to subscribe to the Substack. I figured it was better to stop writing about these companies before I say something that would get me in trouble.

But what happened today with Stride is too interesting.

Jeff Silber at BMO published a research note saying that Roscoe Collegiate ISD elected not to renew its contract with Stride/K12 for Lone Star Online Academy (LSOA). I believe that LSOA represented close to 5% of Stride’s revenue in fiscal 2025. Stride’s stock consequently sold off sharply, close to 15%.

That kind of move gets your attention when you own the name, as I do.

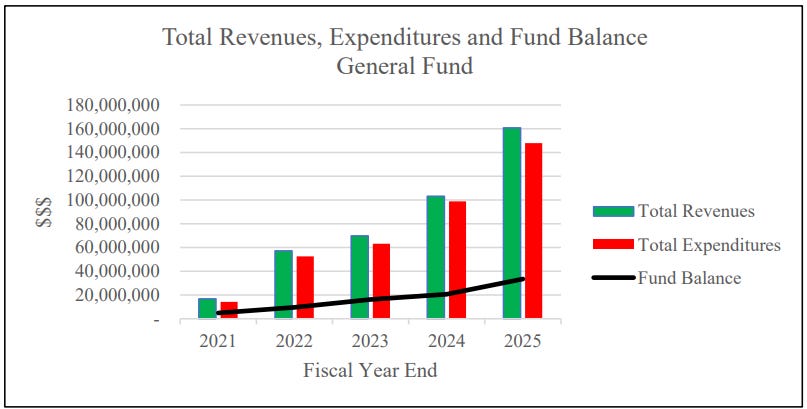

LSOA meaningfully drove revenue growth for Roscoe Collegiate ISD. In 2021, Roscoe generated less than $20M of revenue. By 2025, the district generated revenue of roughly $160M. Most of that increase appears tied to the growth of the virtual school program.

The district’s fund balance also increased dramatically, from a negligible amount to close to $40M.

So the obvious question:

Why would a school district close a school from which it financially benefited?

The general public currently doesn’t know why.

This Wasn’t a Contract Renewal Failure, They Shut Down the School

It would be one thing if Roscoe Collegiate simply decided to use another vendor for virtual school services. But that isn’t the case here. The district didn’t decide to bring the program in-house, keep the students, and eliminate Stride as the third-party provider.

Instead, Roscoe Collegiate appears to have shut down the school entirely.

School districts aren’t usually in the habit of voluntarily giving up enormous revenue streams.

The obvious candidate for explaining the closure: efficacy.

Academic outcomes have always been an issue hanging over the growth of full-time virtual schools. The post-pandemic period didn’t produce just measured enrollment growth. National enrollment almost doubled. Families wanted alternatives. The pandemic legitimized this modality of instruction. Awareness of the offering increased. State legislators increased access.

But with any innovation and societal advancement, haters gonna hate.

Sector critics certainly have always had a long list of complaints about virtual schools. Critics argue that: high student mobility results in weak academic results; virtual schools struggle with math instruction; graduation and persistence rates are low; financial benefits can accrue to districts and vendors at the expense of student success. There are a lot of other complaints, let the record show.

Not every criticism is fair, but these criticisms can’t be dismissed either.

A virtual school can prove financially attractive for a small district and unsustainable if the academic outcomes are too weak.

LSOA appears to be a case study in that tension.

Lone Star’s Academic Profile Was Awful

I acknowledge that awful is a strong word. But that’s the best word to describe the situation.

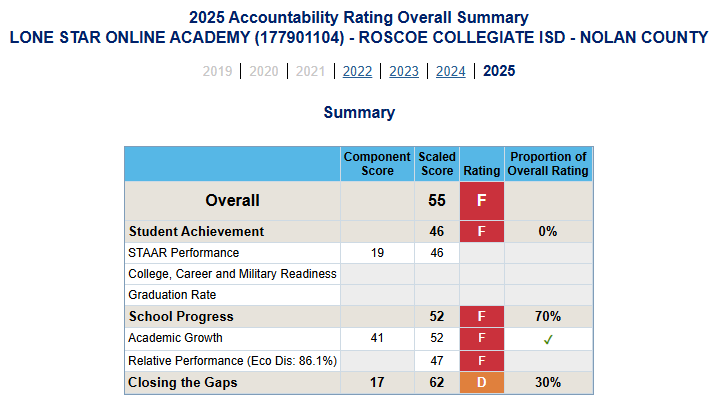

The Texas Education Agency (TEA) has an A-F Accountability Rating System. TEA assigns ratings to Texas districts and campuses based on state accountability domains, including: Student Achievement; School Progress; Closing the Gaps; and Overall Rating.

For 2025 TEA gave LSOA an overall F.

The school received an F for Student Achievement. It received an F for School Progress. It received an F for Relative Performance. It received a D for Closing the Gaps.

In 2024, the picture was even worse, with every rating an F.

The school demonstrated overall Fs for the past three years. Every year that it had a rating.

The most damning metric was Relative Performance.

Relative Performance is a measure that asks: given the percentage of economically disadvantaged students at a school, how does that school’s academic performance compare with other Texas schools serving similar student populations?

That is an interesting metric because it addresses a common defense of low-performing schools. In for-profit education, defenders often argue that it’s unfair to critique raw outcomes without considering the population being served. A school serving a high-poverty highly mobile student population should not be compared simplistically with a wealthy suburban school serving stable students who arrive at grade level.

Relative Performance supposedly adjusts for this.

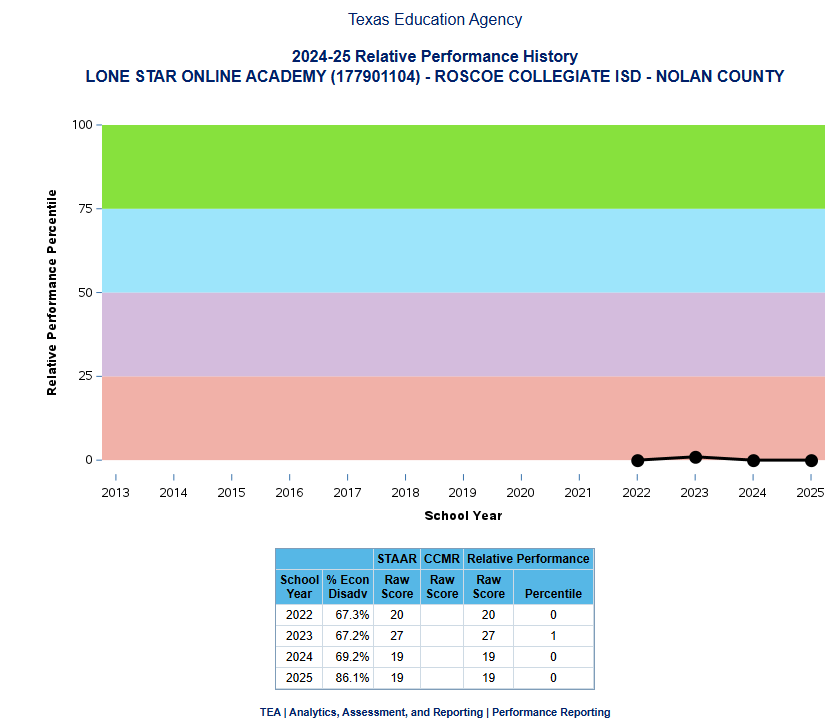

In 2025, Lone Star Online Academy had an economically disadvantaged population of 86.1%. Its Relative Performance percentile was 0.

A 0th percentile result means the school was at the bottom even compared with other Texas schools serving similarly disadvantaged populations.

For years, the bear case on K12/Stride was that virtual schools produced poor academic outcomes and would eventually face political or regulatory pushback. While we still don’t know why LSOA closed, I think it’s fair to ask whether academic performance played a role.

My understanding based on this article from the Texas Tribune is that under Texas’s accountability framework, five consecutive unacceptable ratings can trigger severe remedies, including campus closure or appointment of a board of managers for the district.

The Problem With State Accountability Frameworks

This is where the analysis becomes more complicated than saying, “the school got an F, therefore the school failed.”

How should we define failure?

Texas’s A–F accountability system was designed around a traditional school model. Students enroll at the beginning of the year, attend the same school throughout the year, receive instruction in a structured environment, and then sit for state exams.

Virtual schools serve students who are in transition. Some enroll after the school year has started. Some transfer in because something has gone wrong in a traditional school. Some are behind academically before they ever log into the virtual platform. Some are dealing with anxiety, bullying, health problems, family disruption, neurodivergence, or other challenges that made the traditional school environment unworkable. Some stay for a short period of time and then leave.

This is what’s known as a self-selected population.

If a student arrives in February two years behind in math, takes the STAAR exam a few months later, and does not meet grade level, the accountability system registers that as a failure of the school. The framework is much better at measuring point-in-time proficiency. It can tell us whether students are at grade level. It is less effective at telling us whether a virtual school stabilized students who were previously disengaged, improved attendance for students who had stopped attending, helped students recover credits, reduced family stress, prevented students from dropping out, or created a workable educational environment for students who could not function in a traditional setting.

That doesn’t mean Texas should ignore poor academic results at schools like LSOA.

But it does mean that the score in itself raises questions rather than just answering them.

Repeated F ratings in Texas are not just reputational. They put a campus into an escalating intervention framework. By the third consecutive unacceptable rating, a campus is dealing with formal improvement and turnaround obligations.

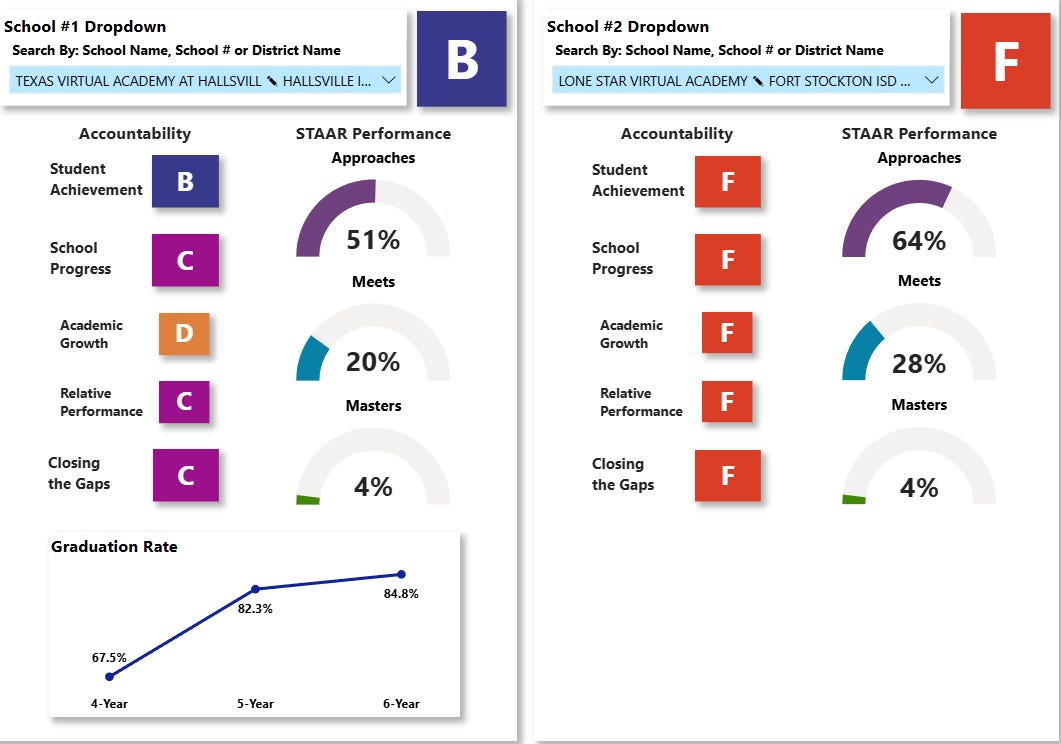

It’s worth noting that the largest virtual school in Texas, another client of Stride named Texas Virtual Academy at Hallsville has a significantly superior academic profile than LSOA.

I haven’t been able to find materials online that explain exactly the academic challenges at LSOA. Did it grow too quickly post-pandemic? LSOA launched in 2020, during the pandemic-era surge in demand for virtual schooling. Currently it has perhaps over 14K enrollments. Both schools use the same curriculum. Have the same management company supporting the school.

One key difference is that LSOA serves students in grades K-8 while the Texas Virtual Academy at Hallsville serves students in grades 3-12. Another is that the students at LSOA are more economically disadvantaged. At LSOA, 86.1% of students are economically disadvantaged, versus 55.4% at Hallsville. That represents a huge disparity.

Education is often about inputs rather than outcomes. Was that the case here?

What the Loss of Lone Star Means for Stride

There are two issues at play here for Stride:

the financial profile of the company

the level of risk associated with future school closures due to efficacy

Stride generated over $2.4B of revenue last year. Roscoe’s FY2025 audit references roughly $134M of fees related to the virtual school agreement. I assume most of that was related to Stride/K12 services. This represented over 5% of Stride’s total revenue.

This creates a revenue headwind, complicates the FY2027 growth story, and raises the question of how much of the enrollment can be retained elsewhere in the Stride ecosystem.

Some LSOA students may migrate to other virtual options in Texas. Texas Virtual Academy at Hallsville is the obvious candidate because it is another large Stride-supported school. If a large number of LSOA students migrate to Hallsville, Stride may retain some revenue, but it may also increase customer concentration in another large Texas program.

Based on TEA enrollment data and Stride’s reported enrollment base, I estimate Hallsville represents roughly 8% of Stride’s reported enrollments. If Hallsville absorbed a meaningful number of LSOA students, increased customer concentration introduces increased risk.

The bigger question is whether Lone Star is isolated or indicative of a broader post-pandemic efficacy problem.

How many virtual schools grew rapidly after the pandemic without building the academic systems needed to support that growth? How many districts became financially dependent on virtual school enrollment while academic outcomes deteriorated? How many other programs are vulnerable if state accountability pressure increases?

That is what today’s selloff is really about. At least in my opinion.

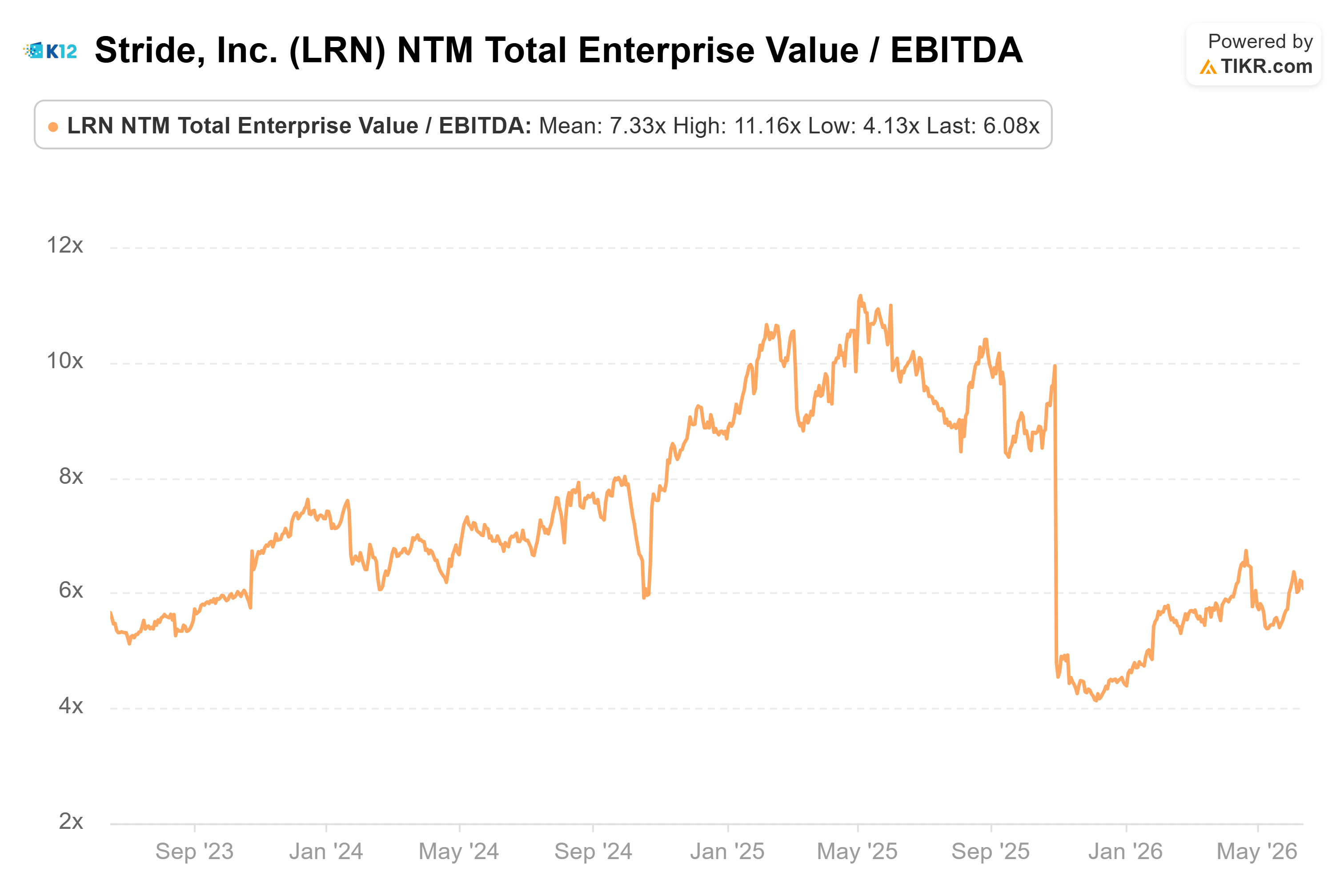

Valuation Still Discounted from Last Year’s Heights

It’s easy to forget, but this has been a challenging year for Stride. The stock declined by 50% last summer given a challenged learning management system implementation which affected the student experience and retention rates. Valuation remains inexpensive at 6x EV/EBITDA. I don’t see that much more room for the stock to collapse given the company’s strong cash flow generation, market leadership, and general market growth.

That being said, the uncertainty regarding the implications from Lone Star may cap price appreciation this summer.

Conclusion - Renewed Focus on Efficacy Key

Virtual schools can be incredibly valuable for the right student. They can also produce terrible aggregate academic results. They serve children who have been failed by traditional schools. They can also become politically vulnerable when state data says those children still are not learning enough. They can generate attractive economics for districts and vendors. They can also become unsustainable if outcomes do not improve.

The closure of Lone Star is a reminder that in education, the financial model only works if the educational model is defensible.

The investment question is whether Lone Star is an isolated local failure or evidence that rapid post-pandemic virtual-school growth created efficacy issues that have not yet fully surfaced.

I don’t know the answer. I still own the stock.

Disclosure / Disclaimer: I own shares of Stride, Inc. This piece reflects my personal views and is not investment advice, a recommendation to buy or sell any security, or a complete analysis of Stride’s business, valuation, or risks. I may change my views or my position at any time without updating this note. The discussion of Lone Star Online Academy, Roscoe Collegiate ISD, and Texas accountability data is based on publicly available information and my interpretation of that information. I do not know the definitive reason Roscoe Collegiate ISD elected not to renew its contract with Stride/K12, and nothing in this piece should be read as asserting a definitive causal explanation unless explicitly sourced.

So, what % of your portfolio is Stride?

Check this news article: https://www.houstonchronicle.com/news/houston-texas/education/article/virtual-school-closes-abruptly-22319484.php