What Happens When Schools Leave Stride / K12?

Case studies of what actually happens when schools in-source from an Education Management Organization like Stride or Pearson

Schools that leave Stride / K12 often expect to operate more effectively outside the EMO model. The data shows a different outcome. Across multiple case studies, schools that separate from their EMO face enrollment declines, execution challenges, and financial pressure. This analysis examines what actually happens after the transition.

TL;DR

This article examines what happens after virtual schools terminate their management contracts with Stride/K12. Literature historically focuses on drivers for schools leaving but ignores what happened afterwards.

Across observable cases, schools face enrollment declines, execution issues, and financial pressure after separating from Stride.

Enrollment loss is the most consistent outcome, not just in the following year but over the long-term. In multiple cases, students appear to shift to other K12-powered schools in the same state, suggesting family affiliation with the platform and curriculum, not the institution.

Replacing the operating stack isn’t impossible but has proven challenging. Schools must rebuild curriculum, technology, and operations. Agora’s attempt ten years ago led to a $20M impairment charge for unusable computers and abandoned curriculum/technology development.

Marketing and demand generation by Stride are underappreciated based on departing schools’ track record. Stride provides enrollment infrastructure and brand recognition that schools struggle to replicate after leaving. Marketing traditionally has not been a needed competence in K-12 education.

Commonwealth Charter Academy (CCA) represents a successful transition from an EMO (Pearson’s Connections Education), but even it likely could not replicate its success in the current funding environment. While CCA in Pennsylvania is often used as a model for independence, it succeeded because of a specific high-funding state environment that is now under heavy government scrutiny.

Bottom Line: There may be good reasons to leave an EMO, but there are many examples of challenges and few success stories.

While leading the strategy function at Pearson’s Connections Education, I believed that Education Management Organizations (EMOs) that serviced virtual schools would eventually make themselves obsolete. I saw that we would help a school reach a critical mass of enrollment and balance sheet surplus at which point the school board would inevitably choose to in-source capabilities. For the past several years, I assumed that the sizeable enrollment growth driven by favorable pandemic tailwinds would finally cause the customer attrition I had warned about for so many years.

While some customers have left over the years, Stride’s model has proven far more durable than I expected.

A decade ago, Stride generated less than $1B of revenue. Wall Street analysts now expect Stride to generate over $2.5B in fiscal 2026.

That disconnect between my hypothesis and reality raised my question: why aren’t more schools leaving?

I addressed this to some degree in my last piece regarding Stride’s positioning given the rise of artificial intelligence. Given the shift from clicking on links to getting synthesized answers from large language models (LLMs), the K12 brand in my opinion has greater value given how AI surfaces schools affiliated with the company and its curriculum.

But my analysis missed an important dimension, something I realized after conversations with former ex-Pearson colleagues.

No one focuses on what happens after a school leaves.

Do schools stabilize or struggle? Do enrollments hold or decline? Do expected financial benefits materialize? Do execution issues occur? Does leadership regret their decision to leave?

There are only a limited number of observable cases where schools have exited an EMO and where industry participants have evaluated outcomes through public data. This piece focuses on those cases. Not to critique those decisions, but to understand the operational and financial consequences that followed.

To be clear, each school operates under its own constraints. Leadership likely had valid reasons to pursue exists from EMO relationships. In the past these have included cost, control, service issues, academic outcomes, and governance.

This is a post-mortem based on observable outcomes: financial statements, enrollment trends, and public disclosures, including board materials where available.

The Structural Drivers of Financial Decline

Publicly available evidence suggests that when a school leaves Stride, the financial profile typically weakens, and not just in the first year. Based on my experience in the industry, this results from three specific operational headwinds:

Competition with Other K12 Schools in the State: Unlike traditional schools, virtual schools do not have a monopoly. Parents choose among options. When a school leaves the K12 ecosystem, it often competes directly against another K12-powered school in the same state. Families who value familiarity and perceived reliability may choose to remain within the K12 system.

Marketing and Enrollment Leadership: Stride operates a centralized scaled marketing engine that is extremely difficult to replicate at the individual school level. While schools can manage daily teaching operations and logistics, generating consistent enrollment is a different skill set that few in the K-12 world know. K12 executes this at a level most schools cannot match.

Operational Execution: Leaving an EMO requires replacing a fully integrated operating model. This includes curriculum, technology platforms, student information systems, vendor coordination, and staffing across multiple functions. Schools have to excel at each one of these functions. The basis of Stride’s success is that it can actually do so, with demonstrable success across multiple states and schools. In practice, individual schools struggle to execute across all of these functions at once, particularly during the transition period.

Why This Analysis Prioritizes Financials Over Academic Outcomes

This analysis focuses on financial and enrollment performance rather than academic outcomes.

That isn’t because academic outcomes are unimportant. It’s because evaluating efficacy in virtual schools is a far more complex challenge than one would think at first blush. By contrast, income statement performance and enrollment trends are observable, comparable, and easier to interpret across schools.

The complexity regarding evaluating academic outcomes relates largely to the non-traditional student population that virtual schools serve. Many families enroll after experiencing a material disruption that warrants a departure from a traditional school: academic struggles; bullying; health issues; attendance problems; or family instability. Traditional schools draw students from a geographic base but are otherwise a randomly assigned cohort. Virtual school students are a self-selected population, often already behind or disengaged at the time of entry.

That reality makes standard metrics difficult to interpret. Proficiency rates and graduation rates are level-based measures. They capture where students are, not how much progress they have made. For a population that starts behind, a school can improve outcomes meaningfully and still report weak proficiency. Differences in student composition further distort comparisons across schools.

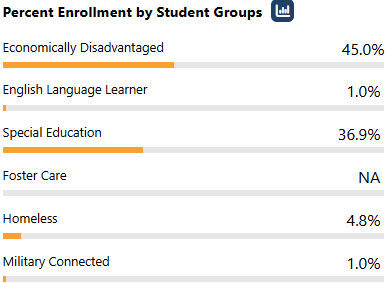

For example, Agora Cyber Charter School, which altered its relationship with Stride / K12, serves a materially higher proportion of special education students. Special Education students represent 37% of total students vs. the 21% of public school students who receive services with IEPs in Pennsylvania. 1.89% of the student population is homeless. For Agora it’s 4.8%. Is it fair to evaluate Agora on traditional metrics like graduation or state test scores?

Conceptually, growth relative to a student’s starting point provides the correct framework for evaluating efficacy. But doing so requires student-level longitudinal data—prior achievement, baseline performance, and duration of enrollment—which isn’t available in public disclosures. Without that data, it’s difficult to isolate whether changes in outcomes reflect operator performance, curriculum quality, or shifts in student mix.

The US Government Accountability Office (GAO) in its 2022 report supports my perspective. The GAO found that full-time virtual schools enroll higher proportions of at-risk students and that available outcome data doesn’t adequately control for those differences. As a result, comparisons to traditional public schools and conclusions about school performance become difficult to interpret. States continue to rely heavily on proficiency and graduation rates, but those measures do not capture student starting points or progress. In practice, even formal accountability frameworks do not allow anyone to isolate whether outcomes reflect the operator, the curriculum, or the underlying student population.

From a regulatory standpoint, what ultimately matters is whether a school meets state accountability thresholds and avoids closure. That is a different question from isolating the impact of a change in operating model.

For that reason, this analysis focuses on financial performance and enrollment trends. While imperfect, these metrics provide a clearer and more comparable signal of how transitions away from EMOs have actually played out.

Case Study: Insight PA Cyber School

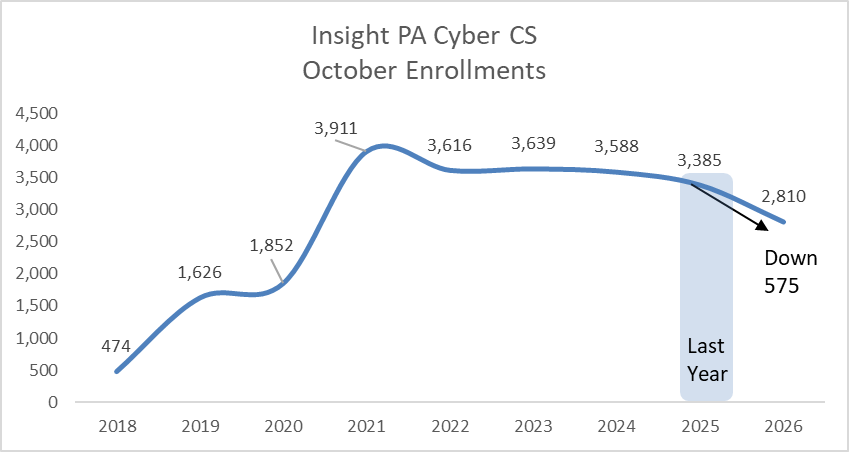

Insight PA provides the most recent example of a school in-sourcing capabilities.

The school launched in the 2020–21 academic year as Stride’s managed school in Pennsylvania, several years after Pennsylvania’s Agora Cyber Charter School reduced its dependence on Stride. The board terminated its relationship with Stride altogether for the 2025–26 academic year.

The timing of the divorce worked against them.

The transition to independence coincided with a reset in Pennsylvania’s funding framework for virtual schools. In November 2025, the state reduced funding by an estimated $178M, followed by a proposed additional reduction of roughly $75M in early 2026. Pennsylvania had historically been one of the most favorable funding environments for virtual schools, so some level of correction was inevitable.

In the first year operating without Stride, Insight saw a decline of 575 October enrollments.

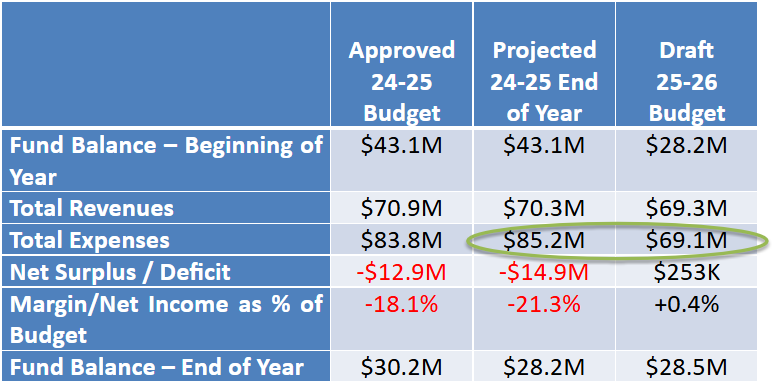

The latest board material from Insight shows management projecting an operating loss of $10M for the year driven by lower than expected enrollments and the revised state funding profile. Cash declined from roughly $25.9M as of June 30, 2025 to $14.7M by March 31, 2026, with an expected year-end balance of around $12M.

In its 2023–24 budget, Insight management outlined an aspiration to move certain functions in-house over a one- to three-year period. That included hiring a chief technology and information officer, system analysts, recruiters, enrollment liaisons, and registrars.

The board materials do not identify a single driver for the transition. They repeatedly reference the school’s large fund balance. Management planned to deploy that balance for strategic investments while reducing its size, noting that regulators and the media could scrutinize it. That scrutiny has since materialized across Pennsylvania.

What stands out to me as a corporate finance professional are the assumptions that management provided in their 2025-2026 budget preview. Management projected $16M of cost savings, $8M of which would come from terminating the relationship with K12. The materials don’t explain where the other $8M comes from, which I find curious. That projection didn’t assume a decline in revenue.

The revenue assumption looks aggressive.

The financial case for leaving Stride looks attractive if costs fall and revenue holds. That framework ignores Stride’s role in demand generation. The K12 brand and marketing infrastructure drive enrollment, and schools cannot easily replace them. Assuming stable enrollment in the first year after separation ignores what other case studies show.

Across the examples reviewed in this piece, schools that leave Stride tend to experience enrollment declines. That pattern suggests the more conservative starting point is the opposite: assume disruption, not stability.

The intended use of the fund balance also becomes relevant in hindsight. Rather than being deployed purely for strategic investment, it has effectively served as a buffer against enrollment declines and funding pressure. As of March 31, the fund balance had declined to $14M.

The broader takeaway is that school stakeholders underappreciate the value of Stride’s platform. Families appear to have an affinity not just for the school, but for K12. When a school removes that affiliation, students do not necessarily stay.

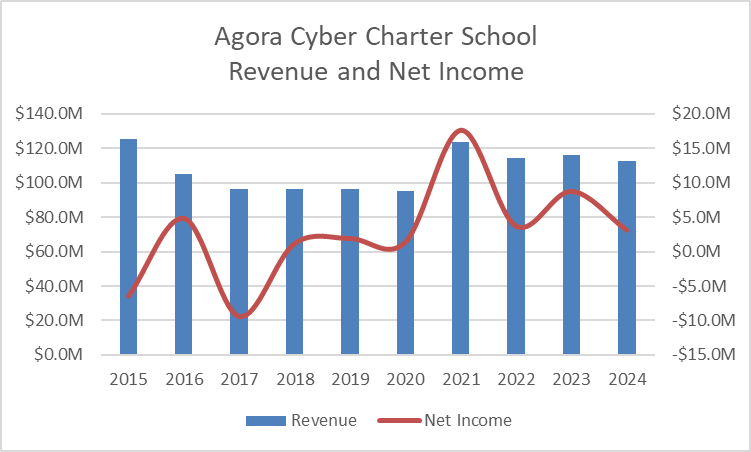

Case Study: Agora Cyber Charter School

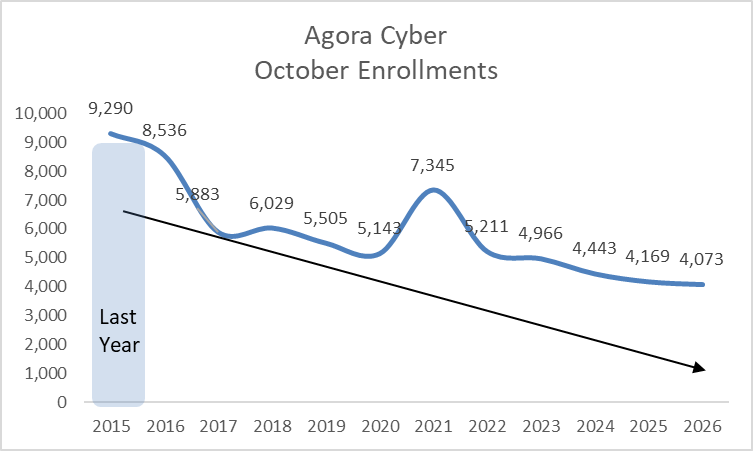

Agora Cyber Charter School launched in 2005 and scaled rapidly. Within less than a decade, enrollment exceeded 10,000 students by 2014, making it one of the largest virtual schools in the country.

In 2014, Agora’s board voted to alter its relationship with Stride. That decision included contracting with new vendors for core capabilities like student information systems, learning management systems, and hardware by 2015. Agora attempted to unbundle and replace a fully integrated operating model.

At the time, Agora stood as Stride’s largest customer. In fiscal 2015, it represented 14% of Stride’s revenue, contributing $129.8M. When the relationship changed, that revenue declined to $18.5M the following year as Agora moved away from a fully managed model and retained only certain services, including curriculum. Stride’s revenue declined from $948.3M in 2015 to $872.7M in 2016, and operating income fell from roughly $18M to $14M. The stock price reflected that disruption, declining from around $40/share to closer to $10/share.

After separating from Stride, Agora lost nearly half its enrollment. The pandemic temporarily boosted student counts, but the long-term trend remained negative. Some might attribute this to a more aggressive competitive landscape. A look at Commonwealth Connections Academy (CCA), a former partner of Connections Education in the same state, offers a telling contrast. Despite also choosing independence from its EMO and starting with a similar base of 8,768 students in the 2014/2015 school year (roughly 500 fewer than Agora), CCA has since grown its enrollment to nearly 35,000.

From Agora’s perspective, the financial trajectory also deteriorated following the transition. Based on IRS Form 990 data, revenue declined from approximately $125M in 2015 to around $95M in the subsequent pre-pandemic years. Revenue recovered during the pandemic to roughly prior levels but has since declined again to approximately $112M.

The school’s attempted operational transition circa 2015 saw challenges.

Agora partnered with Spider Learning to develop curriculum and with Education Elements to build its platform. Those efforts failed. The school disclosed settlement agreements with both vendors in its 2016 financial statements.

By 2017, Agora’s financial statements indicate that the school had reverted back to using K12 for educational products and administrative and technology services.

The financial consequences of the attempted transition saw Agora record a $10M impairment related to computer equipment acquired under a capital lease that was ultimately deemed unusable. In addition, the school recognized roughly $10M of impairment associated with abandoned curriculum, software, and platform development.

Operating cash flow declined from approximately $30M in 2016 to roughly $2M in 2017.

I haven’t been able to find the latest agreement between Agora and Stride, as to what services that Agora uses. The school still appears on K12’s marketing materials as the only public school in Pennsylvania affiliated with K12.

This case highlights the scale of execution risk. Agora tried to replace an integrated system with internal development and third-party vendors. That effort proved more complex, more expensive, and more disruptive than expected.

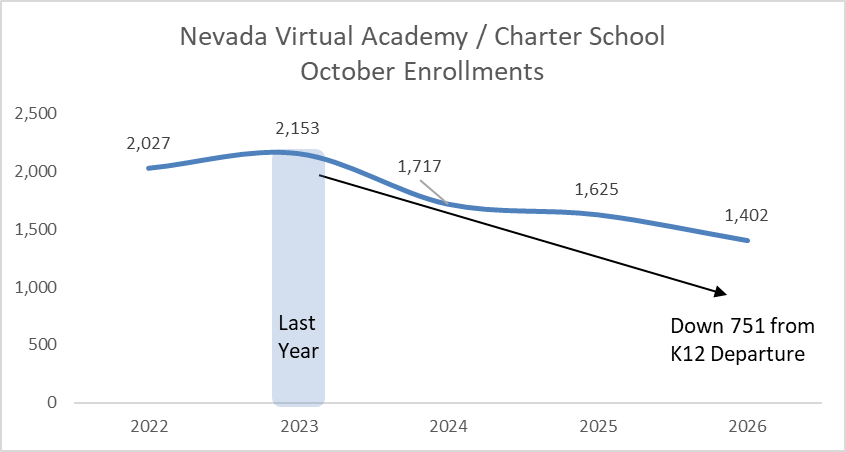

Case Study: Nevada Virtual Charter School (formerly Nevada Virtual Academy)

Nevada Virtual Academy launched in 2007 and operated for years as a Stride managed school. In 2023 the school moved to amend its charter to non-renew its contract with Stride and instead entered a contract with ACCEL for platform and curriculum services. ACCEL was co-founded by Ron Packard, the former CEO and founder of K12.

The board made this decision due to “service and financial concerns with Stride, K12”.

In a contract document explaining the change,

The current EMO has been unable to fulfill service agreements, has caused the school to receive multiple Notices of Concern due to finance mistakes, and was unwilling to be a partner but instead wanted to manage the school. The Board worked closely with SPCSA staff to understand the current and appropriate requirements of an EMO, appropriate pricing structures, and role an EMO should play within the school. Stride, K12’s business/operating model did not support the requirements, and in addition to the failures, the Board decided to non-renew their contract.

As with other cases, the transition itself introduced disruption. After terminating the contract, the school changed its name because Stride retained the rights to the prior name and acronym. There were also claims that K12 contacted families and notified them that they had been withdrawn from the school. While I cannot independently verify the specifics, the school attributes part of the disruption to communication issues during the transition.

The school estimates that it lost approximately 500 students who had previously indicated they intended to return for the 2023–24 academic year.

Enrollment has declined since the transition. State October enrollment reports show a drop of 750 students through the current academic year. The school attributes part of that decline to a charter change that limited enrollment to Clark County, as well as to broader statewide enrollment pressure.

The financial data does not reflect this enrollment decline linearly. Revenue was $18M in 2023, increased to $23.7M in 2024, and then declined back to $18.8M in 2025. The school’s fund balance increased materially, rising from $3.5M in 2023 to $14.5M in 2024.

I can’t reconcile the financial and enrollment data, so I’m reluctant to draw conclusions given my uncertainty about the data. On its surface, revenue and fund balance improved in the near term, even as enrollment declined.

At minimum, the transition created enrollment pressure without producing sustained financial growth.

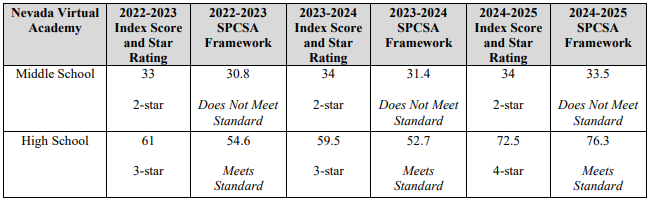

Regarding academic outcomes, the high school showed some improvement under the state accountability framework, while the middle school continued to receive a “does not meet standard” designation. Given the enrollment decline and multiple simultaneous changes, the data does not support a clear conclusion about the impact of leaving Stride.

Case Study: South Carolina Virtual Charter School (SCVCS)

South Carolina Virtual Charter School launched in 2008 and ended its partnership with Stride Inc. (K12) on June 24, 2022.

The transition created immediate challenges.

Around the time of the separation, SCVCS posted on Facebook to address confusion among families who had received emails from K12 indicating that students had been withdrawn from the K12 system. The school needed to clarify enrollment status during the transition, which suggests communication breakdowns at a critical point in the cycle.

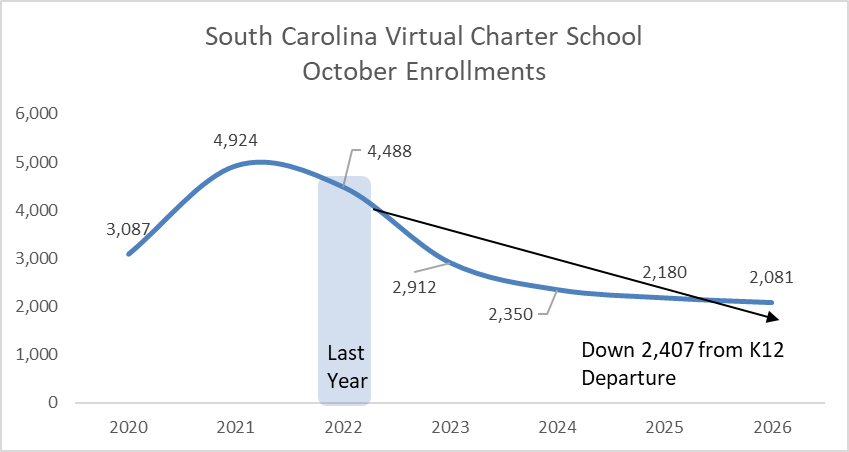

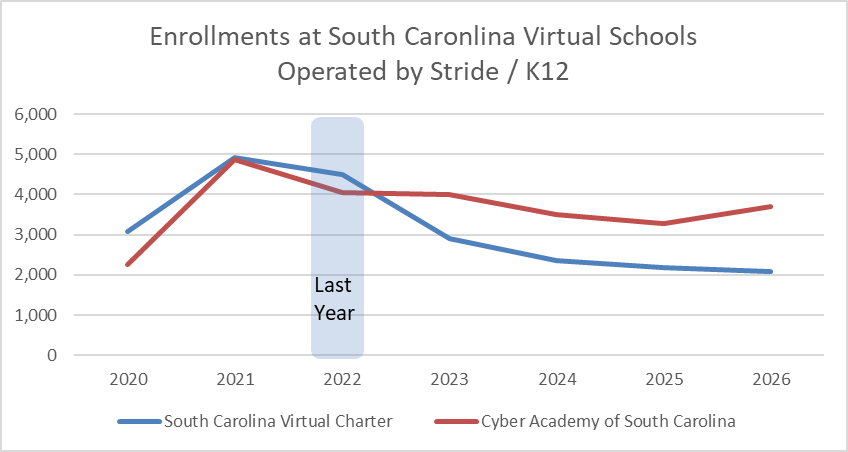

Enrollment data shows clear pressure following the separation. SCVCS lost roughly 3,000 students from its pandemic peak. At the same time, K12 continued to operate Cyber Academy of South Carolina in the same market.

In 2021, combined enrollment across both schools totaled approximately 10,000 students. By October 2026, that figure had declined to roughly 6,000. The K12-powered Cyber Academy lost approximately 1,000 students over that period, while SCVCS lost closer to 3,000.

That divergence suggests share loss rather than a neutral transition. SCVCS exited the K12 ecosystem but continued to compete against the same curriculum, platform, and brand through a remaining K12-powered school. Families who valued that ecosystem had a direct alternative.

Based on IRS Form 990 data, SCVCS generated approximately $37M of revenue in 2022, declining to roughly $26M by 2024.

This case highlights a structural challenge. When a K12-powered school remains in the same state, the exiting school competes against the platform it just left. The enrollment and revenue trends at SCVCS suggest that this dynamic can drive meaningful share loss.

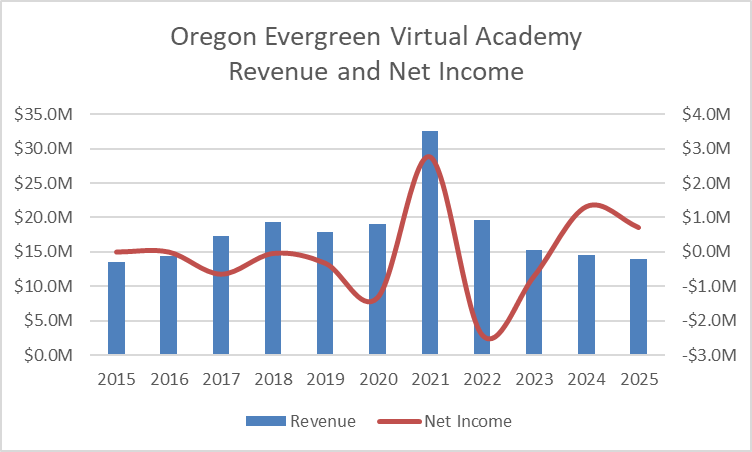

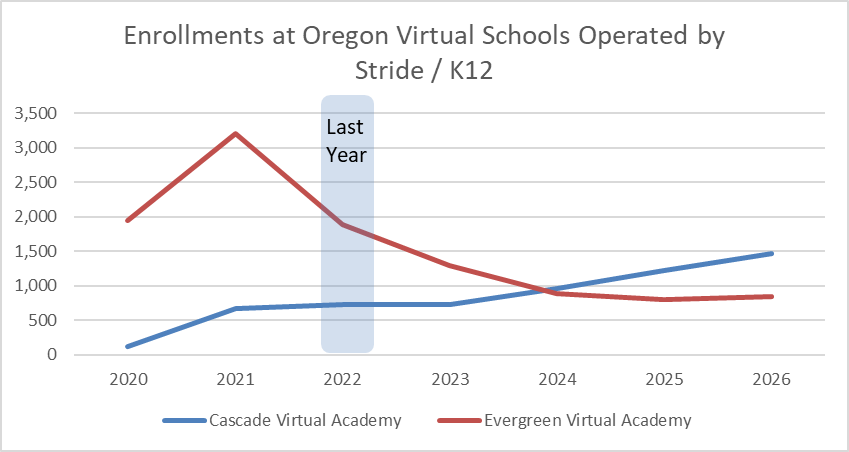

Case Study: Oregon Virtual Academy / Evergreen Virtual Academy

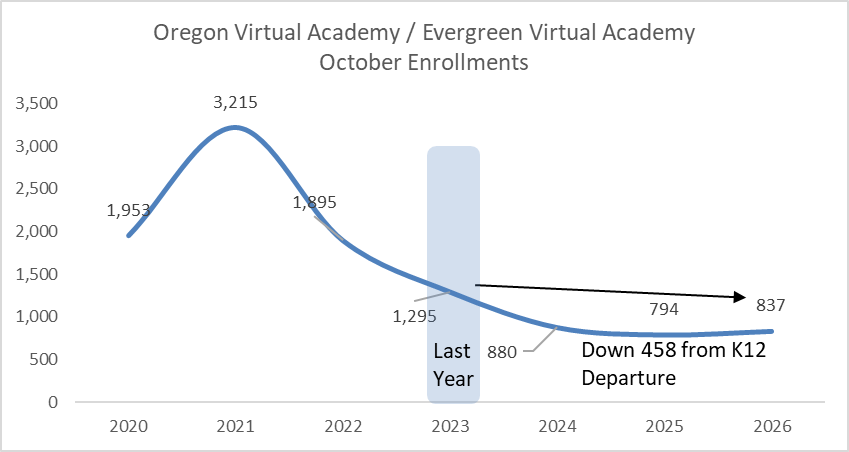

Oregon Virtual Academy launched in 2008 and rebranded as Evergreen Virtual Academy in 2023, reflecting a shift away from the K12 model. The school has not provided a clear public explanation for the transition. Because it operates within a public school district, disclosures remain limited, and most available data comes from IRS Form 990 filings rather than detailed board materials.

The financials follow the same pattern seen in other case studies. Evergreen generated $32.6M in revenue at the pandemic peak in 2021 and then declined to approximately $14.0M by 2025, effectively reversing the entire COVID-era surge.

Enrollment trends moved in the same direction. Evergreen lost students after the transition, while Cascade Virtual Academy—which remains K12-powered—added approximately 739 students over the same period.

Evergreen exited into a market where a K12-powered alternative continued to operate with the same curriculum, platform, and distribution infrastructure. The enrollment divergence points to share loss. Some families likely chose continuity within the K12 system rather than remain with the standalone school.

Case Study: Commonwealth Connections Academy (CCA), the Aspirational Model

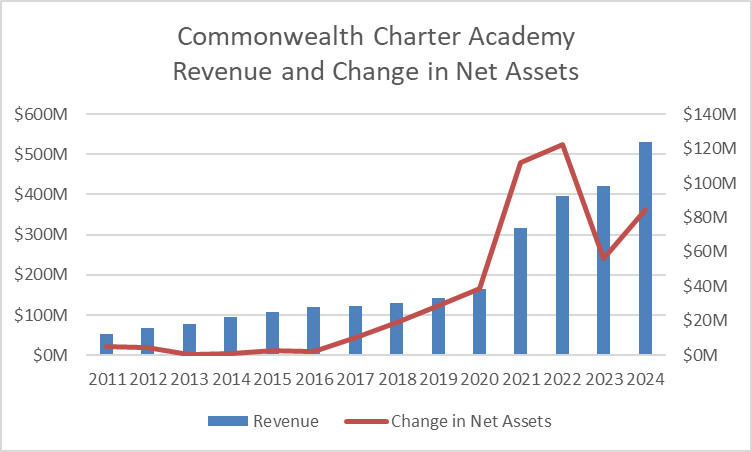

Commonwealth Charter Academy, formerly known as Commonwealth Connections Academy, represents the aspirational case of what a virtual school can become after leaving an EMO. CCA previously partnered with Connections Education and has operated independently for nearly a decade.

Revenue scaled from roughly $50M in 2011 to over $500M by 2024, with the most significant acceleration occurring during and after the pandemic. That growth translated into substantial balance sheet strength. Change in net assets turned sharply positive beginning in 2020, peaking at over $120M in 2022, indicating meaningful surplus generation rather than just top-line expansion.

CCA didn’t replace one EMO with another. It built its own operating model. That includes Edio, a custom platform developed for CCA. It has a fully controlled curriculum with more than 600 courses. It also expanded beyond a pure virtual model into physical and experiential infrastructure. Programs include:

AgWorks – facilities that support controlled-environment agriculture, including aquaponics, hydroponics, and aeroponics

TechWorks - programs focused on robotics, cybersecurity, computer science, drones, and advanced manufacturing

CCA built these programs to integrate career pathways, hands-on learning, and workforce preparation, supported by dual enrollment and external partnerships.

Other aspects of the school:

They offer over 600 educational and social field trips across Pennsylvania.

They have fully equipped mobile classrooms. These are trailer sized vehicles retrofitted with smartboards and science labs to allow hands on learning and face to face interaction.

Source: CCA Website

However, the Pennsylvania Auditor General’s February 2025 report complicates the favorable narrative of CCA. The report highlights that cyber charter schools, including CCA, accumulated large surpluses under the state’s funding formula and deployed capital into significant non-instructional investments. Specifically, CCA spent close to $200M acquiring and renovating 21 buildings, raising questions about capital allocation and public funding levels.

The report argues that the existing funding model allowed cyber charters to retain excess funds rather than return them to districts.

So here’s the takeaway.

CCA’s performance reflects a combination of leadership, funding, and structure.

Leadership: In practice, school performance tracks in lock step with the quality of the school head and board. CCA succeeded because the leadership team not only had a vision but had the capability to execute on that vision.

Funding: CCA operated within a high funding environment that gave management the ability to invest in systems, infrastructure, and program development.

Structure: CCA operates within a single state. That removes the need to maintain fidelity across multiple jurisdictions and eliminates the constraints of a national operating model. Management does not have to standardize across dozens of regulatory regimes, which creates room to innovate.

CCA uses that flexibility to build programs tailored to Pennsylvania. It could develop hybrid models that could incorporate physical infrastructure and experiential learning. That’s something more difficult to execute within a national platform constrained by consistency requirements. A multi-state operator like Stride or Connections prioritizes uniform implementation. This provides advantages to its customers who benefit from best practices and operational optimization. But, this also limits how far any single school can deviate.

That local focus allows the school to design offerings that better match demand and differentiate its model.

CCA demonstrates that leaving an EMO can work, but under a very specific regulatory and funding environment that is now changing. The Pennsylvania government began to scrutinize cyber charter funding and spending in part because of CCA’s performance.

Paradoxically, the very success of CCA — its scale, surplus generation, and capital deployment — may make it harder for future schools to replicate the model.

Conclusion

Schools have valid reasons to leave Stride. Based on conventional statewide academic metrics, virtual schools often lag state averages for reasons discussed in this piece. Boards may perceive their EMOs as rigid because they operate through a standardized model. Boards and school leadership may conclude that they can operate more efficiently or deliver a better student experience by taking control of curriculum and operations.

The case studies point in a different direction. Schools struggle more than expected after they leave. The assumption that an EMO can be easily replaced often proves too optimistic. Schools face execution challenges and lose enrollment during the transition.

Independent service providers target these schools and promote alternatives to the EMO model. That dynamic creates options for EMO customers. Which is fine, all the power to them.

But school leaders and boards should recognize the mixed track record of leaving EMOs.

The financial case for leaving frequently relies on modeled cost savings. Those models should also assume revenue pressure. The key question isn’t whether disruption occurs. Rather, it’s the severity in the first year.

Schools must rebuild curriculum, technology, marketing, and operations at the same time. Each function may look manageable on its own, but coordinating them creates complexity. Stride’s integrated model works because it operates at scale. Schools lose that advantage when they leave.

Schools also underestimate marketing and demand generation. The K12 brand carries more weight than many boards assume. When schools remove that affiliation, they must rebuild demand while competing against other K12-powered schools in the same market. In several cases, students shifted to those remaining options.

Deficit protection adds another layer of value. Stride adjusts pricing to keep partner schools financially viable. Schools lose that flexibility when they leave, and the impact becomes visible when enrollment declines or funding changes.

Taken together, schools that leave should expect lower enrollment, lower revenue, and greater volatility in the near term. They take on full responsibility for execution and lose the stabilizing elements embedded in the EMO relationship.

The termination of a contract creates a difficult separation, with both sides acting in their own interest. That process can be disruptive for students and families in ways that directly impact retention.

Leaving Stride isn’t just a strategic decision. It’s a full operational reset. And based on the evidence we have today, the evidence suggests most schools underestimate how difficult that reset will be.

Disclaimer

I currently hold a position in Stride Inc. (LRN) and may buy or sell shares at any time without notice.

This analysis is based entirely on publicly available information, including company filings, state reports, and third-party data sources. While I have made a good-faith effort to ensure accuracy, I cannot guarantee that all information is complete, current, or free of error. Some interpretations may be incorrect.

This piece reflects my personal views and should not be construed as investment advice or a recommendation to buy or sell any securities. Readers should conduct their own due diligence and consult appropriate advisors before making any decisions.

While I authored this piece, I relied on AI to provide edits.

FAQ: Virtual Schools, EMOs, and Leaving Stride/K12

What happens when a virtual school leaves Stride / K12?

Schools typically face disruption. Across observable cases, schools that leave Stride often lose enrollment, encounter execution challenges, and experience financial pressure in the first year after separation.

Why do schools choose to leave an EMO like Stride or Connections Education?

Boards usually cite control, cost, and flexibility. They believe they can operate more efficiently, customize curriculum, or improve the student experience by bringing capabilities in-house.

Do schools save money after leaving an EMO?

They can reduce direct service costs, but savings often come with trade-offs. Many schools face revenue pressure due to enrollment declines, which can offset or exceed cost savings.

Why do enrollments decline after leaving K12?

Families often associate value with the K12 platform—its curriculum, technology, and brand—not just the individual school. When a school exits the ecosystem, some students shift to other K12-powered schools in the same state.

Is it difficult for a school to replace Stride’s services?

Yes. Schools must rebuild multiple functions at once: curriculum, learning platforms, student information systems, marketing, and operations. Coordinating these pieces creates execution risk.

How important is marketing in virtual education?

Marketing and demand generation are critical. Stride operates a scaled, centralized enrollment engine that most individual schools struggle to replicate. This often becomes a key driver of enrollment declines post-transition.

What is deficit protection, and why does it matter?

Stride’s model includes reducing its fees up until the point that its customer posts a budget surplus. Schools lose that support when they leave, increasing financial risk.

Are there successful examples of schools leaving EMOs?

Yes, but they are limited. Commonwealth Charter Academy (CCA) represents a notable success, but it benefited from existing scale and a favorable funding environment that may not be replicable.

Do academic outcomes improve after leaving an EMO?

The data does not allow for a clear conclusion. Virtual schools serve non-traditional student populations, and available metrics do not isolate whether changes in outcomes result from the operator, curriculum, or student mix.

What is the biggest risk when leaving Stride/K12?

Enrollment loss. Schools often underestimate how much demand depends on the K12 ecosystem and overestimate their ability to maintain stable enrollment during the transition.

Should schools leave an EMO?

Schools may have valid reasons to leave, but they should understand that it is a massive undertaking. It is a full operational reset with real execution and financial risk.

Glad to see you referenced CCA as a one-off success vs. later programs like Reach and Penwood in PA. The high funding was central to CCA's success along with having a good leadership team in place that maintained focus on the student success.