AI’s Impact on Stride/K12(LRN)

LLM discovery strengthens the K12 brand, but AI may require greater investment in curriculum to combat the commoditization of content

TL;DR

Overall, AI is a net positive for Stride. The benefits on the demand side —stronger brand visibility and improved discovery — likely outweigh potential long-term risks from curriculum commoditization.

AI strengthens Stride’s K12 brand. LLM-driven discovery surfaces schools affiliated with the K12 brand and thus improves customer visibility on the web.

AI may erode the value of Stride’s existing curriculum over time. The cost of content creation is collapsing. What was once a core differentiator can increasingly be replicated at low cost, creating a long-term substitution risk.

Curriculum commoditization could drive pricing compression if not managed. If schools can build their own curriculum using AI tools, they gain negotiating leverage.

Stride needs to invest in next-generation curriculum to stay ahead. Stride’s customers have a greater likelihood of renewing at the current fee level if Stride establishes a clear product roadmap explaining what customers will receive. The key question is whether Stride can build an adaptive AI-driven curriculum fast enough to maintain differentiation before any potential pricing pressure.

The durability of Stride’s business model likely remains intact in the age of AI. Stride has a moat. AI can strengthen the moat.

In January, I published an article on Seeking Alpha explaining my thesis as to why investors might want to buy Stride (LRN) stock. At the time, Stride’s challenged implementation of the Canvas Learning Management System (LMS) caused the stock to decline by over 50%. Would Stride’s failure catalyze enrollment churn? Would irate virtual school customers seek to exit their relationship with Stride?

My analysis was grounded in primary research: I reached out to families, scoured parent social media groups, and sat through virtual school board meetings. This is the sort of tedious work that some investors can do, basing an investment thesis on real facts. It led me to the conclusion that Stride’s operational storm had passed and the business had stabilized. Since then, the stock has appreciated by 34%, handily outperforming the S&P 500’s 3% return over the same period.

While the Q2 earnings report put the LMS operational concerns to rest, the current investment conversation on the stock has shifted to a broader and more consequential question: the transformative effects of AI. One cannot conduct channel checks for this sort of thing. Investors are now burdened with speculating about how AI will shift societal norms. How will students learn? How will teachers teach?

Every conversation I have with other investors on LRN inevitably lands on the same question:

How will AI affect Stride — does it still have a durable business model?

Amidst the SaaSpocalypse, a period where AI disruption fears triggered a massive sell-off in software stocks, the question of durability has become the only question worth asking.

What’s being asked of investors requires imagination.

My conclusion: AI could prove a net positive for Stride. But it also carries significant risk if the company doesn’t accelerate investment in curriculum.

While not an existential crisis on par with what some software vendors are facing, AI has eroded the value of Stride’s existing proprietary curriculum. This is definitionally correct. In its last fiscal year Stride invested $22M in curriculum development. Over the past three years Stride invested close to $60M in curriculum development. Given AI tools, how much capital would be required to build the same assets? Probably less.

It’s a leap though to conclude that lower curriculum asset value translates directly into lower enterprise value. Stride is not like edtech provider Chegg that saw a multibillion dollar business collapse over a two year period. Chegg’s end customer was the student, and those users could immediately switch to free alternatives like Google AI Overviews for “homework help”.

Stride operates differently. It signs long-term contracts with virtual schools that buy a bundled solution. Curriculum is only one piece of that bundle. More importantly though, customers aren’t just buying curriculum, they’re buying a system of instruction delivery.

To maintain the company’s market leadership, management must invest further in curriculum to sustain its competitive edge. Failure to do so may result in pricing pressure and customer attrition.

This piece is not a buy or sell recommendation on LRN stock. It is an attempt to answer a specific question: how does AI affect this business? Draw your own conclusions.

I remain long the stock. If I thought AI served as a concern for the next quarter, I would have already sold it.

My Vantage Point: Twenty Years with Stride and the K-12 Virtual School Industry

For readers unacquainted with my background, I was one of the first sell-side analysts to initiate coverage on Stride (then K12 Inc.) when it went public close to twenty years ago.

That work led me to Stride’s chief competitor, Connections Education (owned by Pearson), where I led strategy and later served as general manager of Connections’ institutional business.

My understanding of this company and this industry isn’t guided by financial statements or the curated management commentary found in earnings transcripts. My perspective comes from being in the room when operational decisions were made that moved the needle.

I’ve seen firsthand why boards choose to sign with an Education Management Organization (EMO) like Connections or Stride/K12, and more importantly, why they choose to leave.

I also have a deep appreciation for the historical difficulty of creating curriculum at scale. Building a comprehensive K-12 catalog is a massive undertaking that requires flawless execution. It served as a barrier to entry that has stood for decades. It remains to be seen if AI now threatens to dismantle that barrier.

Why School Boards and Customers Stay With Stride

To understand AI’s impact on Stride, it would be helpful to define the company’s often misunderstood relationship with its customers.

Stride operates primarily as a virtual school provider, servicing both traditional school districts and independent virtual charter schools under its flagship consumer brand, K12.

The student is the end-user.

But the real customer, the entity that signs the multi-year management contract, is the school board or the local district. Stride provides the infrastructure, the teachers, and the curriculum. The board retains governance and accountability.

For years, I believed this model contained a structural flaw: that once a managed school reached scale, it would internalize operations and exit the Stride partnership. That thesis has not played out. Enrollment growth and long contract durations suggest switching is far less common than I expected.

Reasons why schools stay with Stride:

Many schools are financially constrained from switching. Most states provide insufficient per-pupil funding for virtual schools to afford contracting with a provider outside of Stride. Schools often carry a fund deficit that requires Stride to discount its pricing until the school builds a fund balance. Most do not have the balance sheet to in-source.

Execution risk to replace Stride is high. Stride provides a turnkey, compliant, and proven operating model. Replacing that system is complex and time-consuming. It requires building or licensing curriculum, hiring staff, implementing systems, and ensuring regulatory compliance. Most boards are not incentivized to take on that level of operational risk. They are stewards, not disruptors.

Families have loyalty to the K12 brand rather than the school. Stride typically operates several K12-powered schools within a single state. It turns out that parent loyalty does not reside with the local board or administrative authority. It resides with the K12 curriculum. If a specific board attempted to exit Stride, families could and would migrate to another K12-affiliated school in the same state to preserve continuity.

Customer attrition does occur. But when it happens, it’s typically in environments where funding is unusually favorable.

Pennsylvania is a clear example. The state has historically provided among the highest per-pupil funding levels for virtual schools, making independence more viable. Several Pennsylvania schools have exited EMO relationships as a result.

Insight PA Cyber Charter School provides a recent case study. The school exited its relationship with Stride last year.

In its first year independent of Stride, Insight as of October 2025 was 600 students below budget. An enrollment shortfall in itself is a serious issue, but this one coincided in the same year as when Governor Shapiro decided to cut funding for virtual schools in PA. As a consequence, Insight will see a close to $10M deficit. Unfortunately, the challenges required Insight to lay off staff. Insight has not been unique in facing these challenges, other virtual schools in Pennsylvania have laid off staff as well. But had Insight stayed in its partnership, Stride would have reduced its fees to Insight up until the point that Insight maintained a fund balance.

The take-away is that leaving the Stride partnership introduces material financial risk perhaps not acknowledged by stakeholders.

It’s difficult for an external observer to isolate the exact cause of the Insight enrollment shortfall. But one plausible factor is the loss of association with the K12 brand and curriculum.

From a parent’s perspective, the curriculum is often the product. In many cases, K12 is the school.

That dynamic likely explains why families remained with K12-powered schools when the company transitioned to the Canvas LMS.

The type of families enrolling their children at a K12 powered school are trying to fix a problem unsolved by the traditional school system.

For them, K12 isn’t just a consumer product.

It’s manna from heaven.

AI Benefits: Discovery as a New Moat

AI offers three distinct strategic advantages to Stride.

Margin Expansion. Automation of labor-intensive tasks—enrollment, document verification, customer support, back-office support—creates a clear path to leaner operations and improved operating leverage. I’m not sure how big of an opportunity that is though, because management has already invested in these areas over the past several years.

Improved Instructional Efficacy. With the cost of software and curriculum development meaningfully reduced, Stride can create more tools that measurably improve student outcomes. For example AI-enabled tutoring (now in beta mode at Stride) that provides real-time explanations, step-by-step guidance, and reinforcement tailored to each student’s level of understanding, creating a feedback loop between instruction and comprehension.

Strengthening the K12 brand. The most consequential advantage of all.

Historically, education functioned as a localized monopoly, with students attending schools based on residential districting. Prior to the pandemic, virtual schooling itself was not widely understood, and awareness of specific options was limited. Virtual education is now broadly recognized by families as a category. The market has now become crowded. In a state like Ohio, there are fifteen statewide virtual charter schools and over one hundred district-operated online programs.

The question is no longer whether virtual school is an option, but which one to choose.

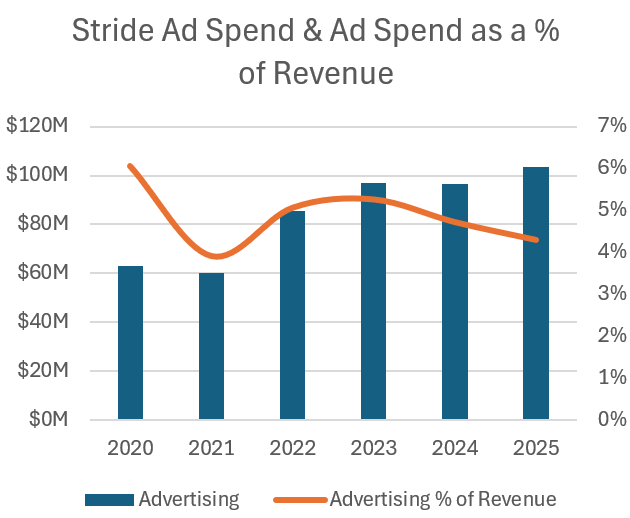

In the past, that decision was heavily influenced by marketing from an education management organization or a virtual school. Schools competed for visibility through search engine optimization, attempting to appear at the top of Google results to get a user to click on a link and drive traffic to a landing page. This was a scalable model to some degree, where upfront investment in SEO could generate incremental enrollments at a low marginal cost. Paid search, bidding on Google keywords, supplemented SEO from an Internet advertising perspective. Yes, the company also invested in direct mail, print media and television commercials, but the presumption is that most of their ad spend was on the Internet.

Given Stride’s scale and the prominence of the K12 brand, ad spend only represented about 4-6% of the company’s total revenue. Presumably a Stride customer would have to pay more in advertising as a % of revenue if they didn’t have access to the K12 brand.

How much would a school need to invest in ad spend today given that AI and LLMs have fundamentally changed how consumer brands are surfaced and become visible on the web?

Discovery is no longer about a family navigating a list of links. It’s now about receiving a synthesized answer. When a parent enters a search today, Google AI Overviews or ChatGPT provides a direct response, and that response privileges sources with established authority across the web.

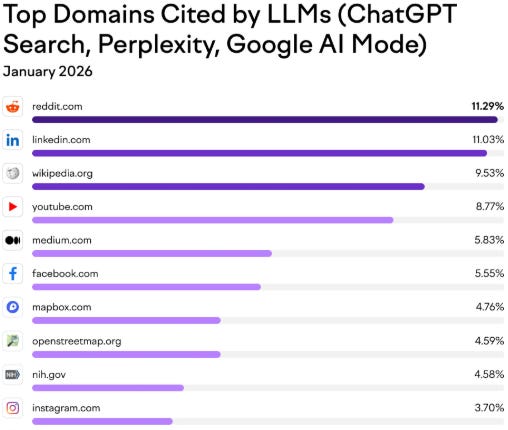

This shift disproportionately benefits brands with a long history of distributed presence across key websites. Stride’s K12 brand has been cited, reviewed, and referenced across the ecosystems that large language models rely on, including YouTube, Reddit, Wikipedia, LinkedIn, etc… That accumulated digital footprint becomes a structural advantage in an AI-driven discovery environment, increasing the likelihood that K12-affiliated schools are surfaced as trusted recommendations.

This dynamic has important implications for customer retention of virtual schools. For a school board, leaving Stride in the past would have resulted in lower enrollment and reduced marketing efficiency. Now though, disaffiliating from the K12 brand could reduce a school’s visibility within AI-generated answers. It’s uncertain how a school can rebuild that authority on the Internet. Because these AI systems operate as black boxes, there is no clear pathway for a new or unaffiliated brand to replicate K12’s positioning.

In that context, the K12 brand evolves from a marketing tool into a defensive moat. In the pre-AI world, discovery was driven by marketing execution. In the AI-driven world, it is driven by accumulated authority. Stride has built that authority over twenty years. It may prove to be the company’s most durable competitive advantage.

School boards will presumably recognize this and, as a consequence, will be more reluctant to sever their affiliation with the K12 brand.

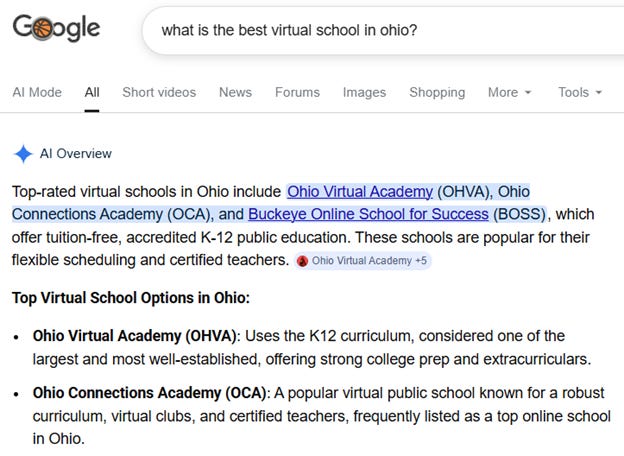

To test this, I asked Google AI Overviews in Incognito mode (to avoid any personalization bias) to identify the best virtual schools in Ohio. The first result was Stride’s Ohio Virtual Academy (OVA). The output specifically cited K12’s curriculum as a hallmark of the school’s quality, describing it as one of the largest and most established in the country.

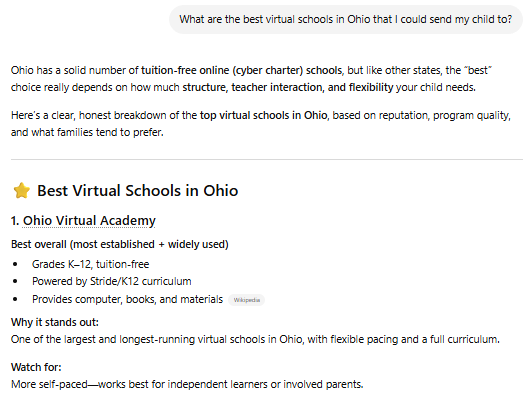

I ran the same experiment on ChatGPT and received a nearly identical result.

The transition to a non-K12 brand could potentially cause a school to disappear from the synthesized answers outputted in an LLM-driven world.

In the AI era, the K12 brand may actually be Stride’s strongest defensive moat.

Curriculum Commoditization: A Risk That Requires Investment

Generative AI introduces a clear strategic risk for Stride by collapsing the cost of educational content creation. What was once capital intensive can now be replicated far more cheaply.

Operating a full K–12 virtual school required a massive upfront catalog. 150+ semester-length courses, excluding electives. At an average development cost of $100K per course, building a proprietary library implies a $15M+ investment. That’s just for the initial roll-out and doesn’t include ongoing maintenance. This sort of prohibitive cost forced virtual schools to rely on third-party providers like Stride. It also limited the number of education management organizations in the market because of the massive upfront fixed cost investment required.

Ten years ago, while working at Pearson, the idea that an AI tool could recreate K12’s curriculum on demand would have sounded like science fiction. Today it’s a legitimate question investors should be asking: when will a large language model be capable of generating a course of comparable quality to K12’s existing catalog without any human intervention in the build process—in 2027? 2028?

If and when that capability arrives, a credible substitution threat exists. If schools can develop their own content, the value proposition underpinning the Stride partnership erodes.

To be clear, Stride provides far more than curriculum. It delivers a bundled suite of services including marketing, enrollment operations, customer support, software, compliance, teachers (in some cases) and administration. Also deficit protection (reducing fees to ensure that a school has a fund balance). But curriculum has always been the core differentiator and the source of brand identity. Any education management organization can operate a school, with varying degrees of success on marketing or compliance. Many schools operate independently. Only Stride can provide the K12 curriculum and its teaching model. As content becomes commoditized, bargaining power shifts toward the customer.

Here’s a good case study to provide some context.

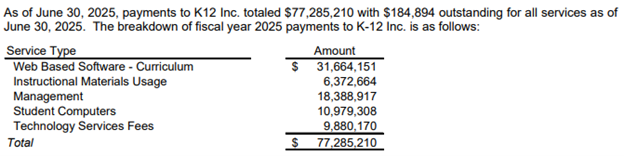

The Ohio Virtual Academy (OVA) serves as one of Stride’s largest customers. OVA serves roughly 16,000 students. Per the school’s annual report, it paid Stride $31.6M for web-based software and curriculum for academic year 2024/2025. This represents nearly 40% of the total fee OVA pays to Stride and 26% of the school’s total revenue. This clearly includes both software and curriculum. The data doesn’t provide the split between the two, so for the purposes of this exercise let’s conservatively assume that digital curriculum is half of the $31.6M, or $15M.

If OVA could hypothetically develop its own curriculum at minimal cost using AI, consider how it might redeploy $15M:

Reduce the student-teacher ratio (at $100K per teacher, $15M equals 150 additional full-time educators)

Create micro-campuses for in-person enrichment

Subsidize paid internships

Fund dual-enrollment college scholarships

Sponsor annual international travel programs

Would a school offering those enrichments be more attractive to parents than one running Stride’s K12 curriculum? Possibly. The more important question is what happens at contract renewal if OVA arrives with a credible AI-generated curriculum and the ability to threaten full in-sourcing. The leverage dynamics shift materially.

Commonwealth Charter Academy (CCA) in Pennsylvania offers a useful precedent. In the 2010s, CCA developed its own proprietary curriculum and severed its relationship with Connections Education. In 2025, CCA generated over $665M in revenue with a $67M operating surplus. Most schools could not replicate that path given funding realities. Could OVA? In 2025, OVA reported a $5M fund balance, meaning it might have the financial cushion to survive a separation from Stride. But as we saw with Insight of PA, a new governor can change funding to virtual schools and just like that a fund balance can turn into a deficit.

The complicating factor is that families likely chose OVA precisely because of K12’s curriculum and pedagogy. Even if OVA in this hypothetical example claimed its proprietary curriculum replacement was superior with better outcomes, how many students would it be willing to lose in the transition? That student retention risk constrains the board’s leverage.

AI Is Different From Open Educational Resources

Some readers will point out that the promise of free curriculum isn’t exactly new. We’ve seen this before in the form of Open Educational Resources (OER). Free content like EngageNY never truly displaced proprietary curriculum. Why would AI be different?

This is a fair point.

OER are teaching and learning materials. Textbooks, lesson plans, videos, full courses, learning modules, etc… They reside in the public domain or are released under an open license (like Creative Commons). This allows anyone to use them without a cost. The analogy to open source software is apt. And like open source software, OER never achieved the displacement that proponents predicted.

One of the reasons why related to the total cost of ownership. Adopting OER required labor-intensive work: mapping free lessons to state-specific standards, training teachers, providing technical support. The savings on content were offset by the cost of implementation.

It’s unclear what the cost of implementation with AI might be. Again, everything I am describing is theoretical.

AI presumably can automate the mapping, the standards alignment, the adaptation to local requirements, etc… The labor costs that made OER impractical possibly apply or possibly don’t in the same way to AI-generated curriculum.

The structural barrier that protected K12’s curriculum was not merely the upfront investment, it was the ongoing operational complexity of deploying it.

The only way we’ll really understand the risk factor associated with deploying an AI generated curriculum is a school actually doing it. To date, I’m unaware of such an experiment.

To Maintain Its Moat, Stride Must Prove Its Curriculum Is Superior to AI-Generated Alternatives

Historically, Stride’s revenue was protected by the sheer capital intensity of curriculum development. To maintain its current pricing power, Stride must demonstrate that its curriculum is fundamentally superior to good-enough AI-generated alternatives.

Stride is unmatched in K–12 edtech at scale. We are talking about a company that may generate over $2.5B in its current fiscal year. That scale gives it advantages in building AI-driven curriculum that smaller competitors cannot replicate.

That scale will be helpful, because as the cost of generating content approaches zero, the investment required to remain differentiated increases.

Stride must build a next-generation adaptive curriculum offering that is personalized, continuously improving, and deeply integrated into the learning experience. Rather than harvesting margin from lower content creation costs, the company may need to sustain or even accelerate curriculum investment to preserve its positioning.

The notion that companies must aggressively reinvest in their products to harness AI is a theme playing out across software and data sectors. Factset, DocuSign, Zoom, and Microsoft have all explicitly tied margin pressure to AI investment. I wouldn’t be surprised if Stride management announced that next year would serve as an investment year in margin for research and development for the next generation of an AI powered adaptive curriculum. To be clear, management has not communicated their intention to do so in any way.

One potential mitigating factor: Stride capitalizes its curriculum development and amortizes it over three to five years. A surge in development spending today might not translate directly into a near-term margin blow. The cost could be smoothed over multiple years.

Management has not yet had this conversation with investors about investing for the future. This year’s focus has been on LMS stability. The risk is that the company arrives at an epiphany about investing only after a major customer announces a departure.

To the extent that management referenced investment in AI, this is what the CEO said in the 4Q25 conference call:

And of course, everybody is talking about AI. We are proceeding with our cautious but ambitious approach to enable the use of AI in our programs in a responsible and impactful manner. I said a couple of years ago that we are not going to play into the hype around AI but rather focus on foundational areas and technologies that we can leverage for better customer outcomes and experiences. And we are continuing down that path both in partnership with other providers as well as through proprietary.

The lack of specificity on investments regarding AI may have been appropriate six months ago. But after the SaaSpocalypse, investors need better answers regarding the company’s product roadmap.

Curriculum development by Stride would likely focus on adaptive curriculum. Stride specifically referenced adaptive learning technologies in its 10-K

Unlike digital courseware, adaptive curriculum could use AI to identify a student’s specific struggle areas in real time. Instead of a linear path from Lesson A to Lesson B, an adaptive system would function as a real-time instructional agent. For example, if a student falters on a concept, the AI identifies the root struggle and branches the student into a custom practice module or triggers a specific teacher intervention.

Stride services over 200,000 students. The company has the financial resources to build proprietary AI-native products and spread that cost across a massive base.

This is how Stride can strengthen its moat.

Investor Sentiment: Is the Market Pricing in an AI Risk?

Because Stride has been navigating self-inflicted operational challenges, the long-term strategic implications of AI may not yet have registered with most investors. The past six months have been dominated by the fallout from the Canvas and PowerSchool implementations.

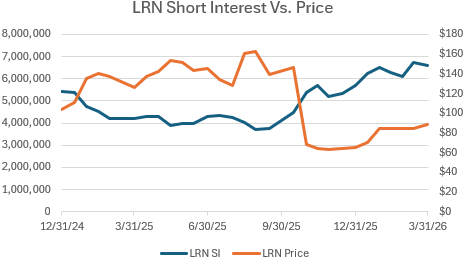

Yet short interest in Stride has increased significantly over that period, climbing from 4.4M shares in late 2025 to nearly 6.6M shares as of March. Short interest as a percentage of the float now stands at 22%, making Stride the 230th most-shorted stock in the market, just ahead of Pinterest.

What’s driving the short position?

Is it a continuation of the operational fallout thesis, now largely resolved?

Or is the market beginning to price in a structural risk, the same AI-driven disruption thesis emerging across software and data companies?

Or maybe it’s something else altogether. Stride has been a target for shorts for years. For-profit education stocks always receive scrutiny.

Conclusion: AI Risk Exists, But It Can Be Managed

In my opinion, the core investment thesis for Stride remains intact in the age of AI.

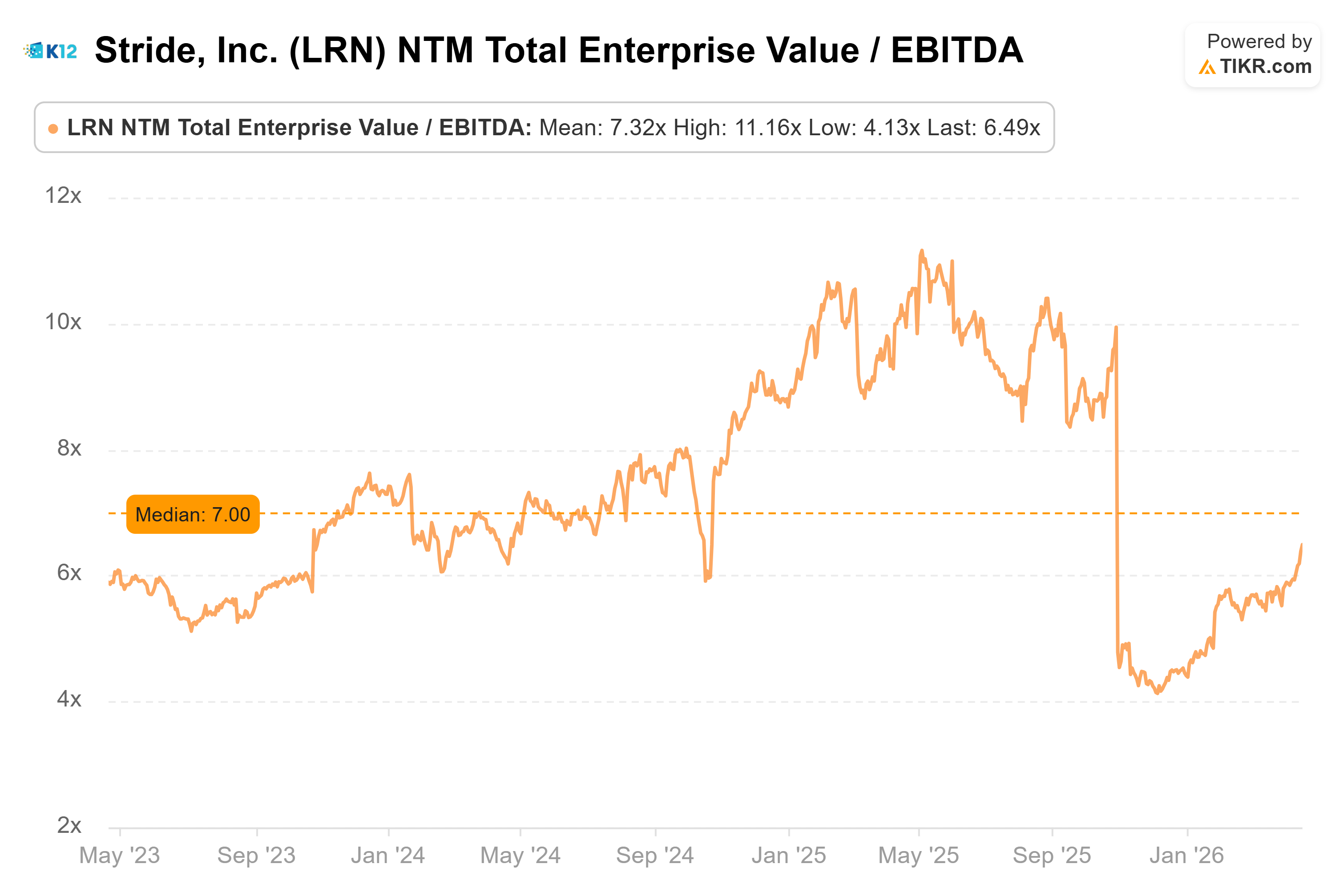

Valuation multiples may expand as investors have comfort that the company has stabilized operations following the disastrous LMS migration to Canvas. Conceivably LRN can once again warrant a 10x EV/EBITDA multiple. Even achieving the historical median multiple of 7x would result in stock price appreciation. It would be helpful if the company posts a good Q3 print in two weeks.

I find it difficult to envision widespread customer attrition in the near term. School boards that endured the fall 2025 disruption are unlikely to subject families to another transition so soon. The switching costs—operational, financial, and reputational—remain high.

So I feel pretty comfortable right now owning Stride stock even with each new headline about AI.

AI likely does not serve as an existential risk for Stride in the same way that it has affected data and services companies.

It does reduce the scarcity value of curriculum and introduces a credible long-term substitution risk if Stride’s product remains static.

Stride likely has time on its side to invest and maintain a product lead over alternatives.

Stride operates under multi-year contracts with school boards. Switching providers is operationally complex. Even if a school believes it can replicate elements of Stride’s offering using AI, the transition would require time, coordination, and a willingness to accept execution risk. That creates a natural buffer.

Pricing pressure, not customer attrition, becomes the first signal of disruption.

The greatest risk is not AI itself, but underinvestment in response to it. If Stride attempts to expand margins by reducing curriculum and software investment, it risks eroding its differentiation at precisely the moment when customers gain alternatives.

Stride has an opportunity to out-invest the competition and ensure that the K12 experience remains the gold standard.

Disclosure: I am long LRN at the time of this writing.

Disclaimer: This is for entertainment purposes only. Do your own research. This analysis is my own and is not intended as investment advice.