How Big Could the U.S. K-12 Virtual School Market Really Get?

Accelerating demand and high penetration rates in certain states suggest that the market could triple from current levels.

The pandemic fundamentally changed assumptions about the size of the virtual school market. Prior to COVID, industry stakeholders viewed virtual schooling as a niche category serving a relatively small portion of K-12 students. But several years after schools reopened, virtual school enrollment growth has accelerated in some states rather than reverting back to pre-pandemic levels. Virtual schooling has now crossed the chasm from a niche offering into a mainstream educational option for families with specific needs. I argue that full-time virtual school enrollments can potentially triple from current levels over time, with policy and regulatory resistance serving as the primary constraint on adoption.

TL;DR

Full-time virtual school penetration could reach 7% in an unconstrained environment, but the regulatory-adjusted market likely sits closer to 5%. Applied to roughly 50M U.S. K–12 students, a 7% penetration rate implies 3.5M full-time virtual students. After excluding states unlikely to permit broad virtual school expansion, the realistic addressable market falls to 2.45M students, or roughly 3.5x–4.0x today’s estimated 600K–700K student base.

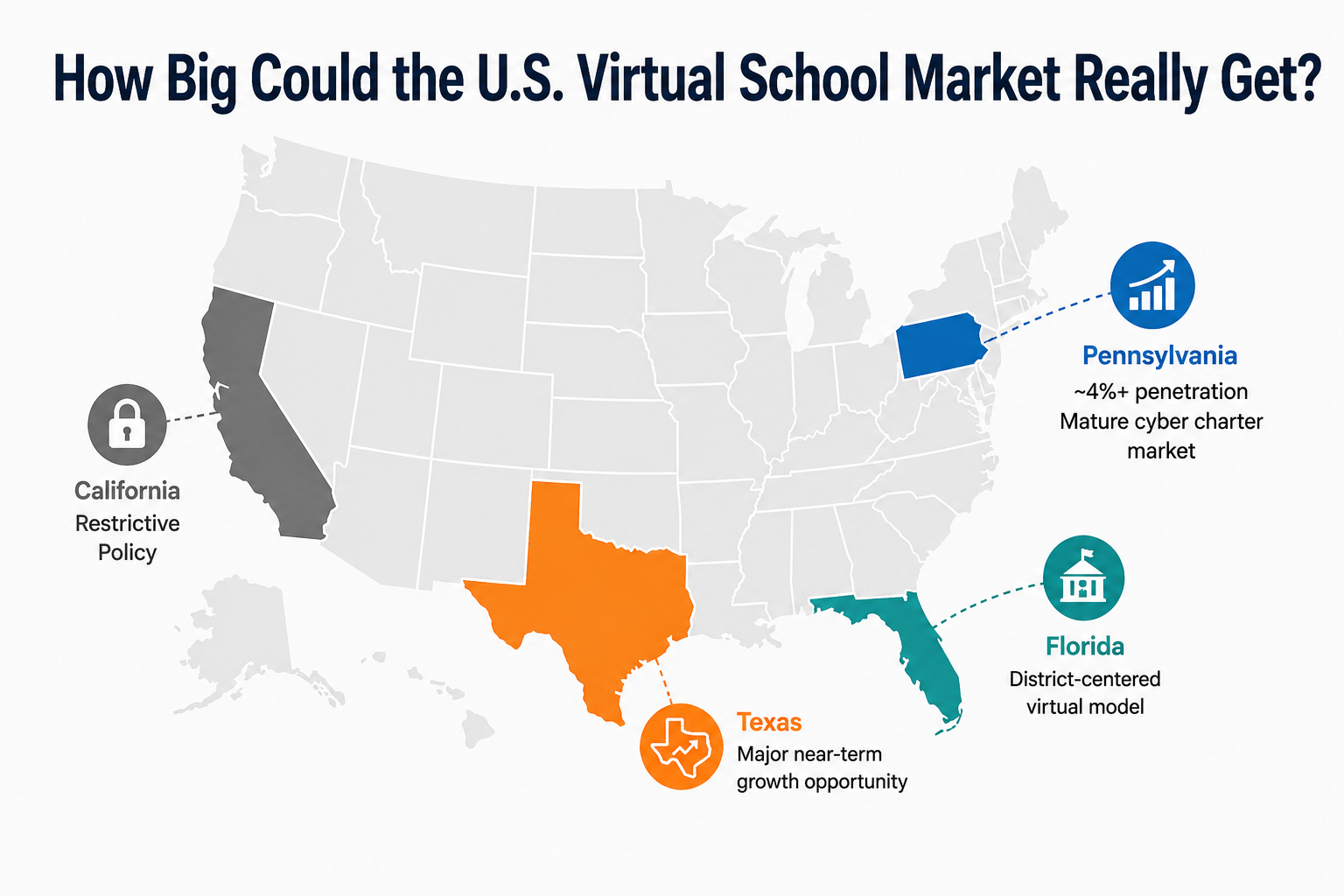

Regulatory resistance likely caps virtual school enrollment growth for 30% of the US K-12 population. States unlikely to permit an expansion of enrollments include California, New York, Illinois, New Jersey, Washington, Massachusetts, Oregon, and Connecticut.

Regulatory hurdles, not a lack of family demand, continue to serve as the primary bottleneck for industry growth. Families have signaled a clear desire for these programs post-pandemic, but restrictive authorization frameworks, oversight rules, moratoriums, and enrollment caps continue to block them.

Growth in virtual enrollments does not automatically benefit education management organizations like Stride or Pearson’s Connections Academy. Each state structures virtual schooling differently. Florida, for example, built a district-centered virtual infrastructure around its own statewide entity, Florida Virtual School.

The virtual school market likely continues impressive near-term growth, particularly with the loosening of rules in Texas. Recent legislative changes removed structural barriers that historically constrained virtual enrollment growth in one of the country’s largest K–12 markets.

AI represents the great unknown, but likely creates further options for families and potentially redefines virtual instruction.

Context: Stride/K12 as the Virtual School Market Bellwether

This concludes my series on the virtual school market and Stride/K12 (LRN). Thus far I’ve written about:

Stride as an investment, published in Seeking Alpha.

As the market leader in virtual turnkey management services, Stride remains the central figure in any discussion regarding the industry’s position.

Stride put the industry in Wall Street’s spotlight back in October. The stock price declined by 50% following a meaningful challenge with Stride’s implementation of a new Canvas learning management system. This operational crisis served as a stark reminder of the Herculean effort to execute virtual school operations successfully. Savvy investors viewed this temporary dip as a buying opportunity for a quality business, especially since the stock had appreciated sixfold since the pandemic.

I’ve spoken with a number of investors in an informal (not professional) capacity over the past six months. For new readers to this newsletter, I served at competitor Connections Education / Pearson as head of strategy for six years including a stint for two of them as general manager of the $60M revenue generating institutional business selling virtual school solutions to school districts. Previously I served as a sell-side analyst covering the stock at several investment banks.

One of the first questions that investors asked when kicking the tires on the name was “how big can this market get”?

My response was usually along the lines of “I have no idea.”

This wasn’t an exercise in humility.

The Addressable Market Falls from 7% to 5% Penetration After Political and Regulatory Constraints

Prior to the pandemic, I used to say that the national addressable market was 3% of the K-12 student population. That full-time K-12 virtual instruction would always be a niche offering within the mosaic of broader K-12 solutions. At that time, in the states with the most progressive regulatory environment, penetration pre-pandemic appeared to peak at perhaps 3%.

For most pandemic related behaviors, consumers reverted back to the status quo.

Not for this market.

The pandemic increased awareness both of the category’s existence and also the capacity for families to benefit from the virtual education experience. Notice how I say family rather than students. Education is a family affair. Understanding this is central to understanding the opportunity with full-time virtual instruction.

I’ve had some time to reflect and research how virtual schools have fared post-pandemic, enough to attempt to answer the question of how big this market can get.

I believe the full-time virtual school penetration rate could eventually approach 7% of the U.S. K–12 population in an unconstrained environment. Applied to roughly 50M public K–12 students, that implies a theoretical market of 3.5M full-time virtual students.

But states dictate K-12 education policy. Some will not allow or support this modality. If roughly 30% of U.S. students live in states unlikely to permit large-scale cyber charter expansion, the regulatory-adjusted penetration rate falls to approximately 5%, or roughly 2.45M students. That compares with today’s estimated 600K–700K full-time virtual students.

Charter school law matters because it created the vehicle that allowed full-time virtual schools to scale. In states that authorized statewide cyber charters, families could leave their local district and enroll in a public online school that served students across the entire state. That gave virtual school operators scale, which allows them to invest further in their schools and market the offering to more and more students. States that allow cyber charters create a path for rapid virtual school growth. Districts can serve virtual enrollments but few have scaled meaningfully — unless they operate through a framework that grants them a statewide purview.

Unfortunately, this market lacks clean reportable data allowing for analysis. The best national estimate comes from NEPC’s 2023 Virtual Schools in the US report, which found that full-time virtual school enrollment increased from 332K students in 2019–20 to 644K students in 2020–21. Because national enrollment declined somewhat afterward but remained far above pre-pandemic levels, I use roughly 600–700K students as the current national market-size range.

Here’s how I come up with the long-term 5% penetration rate.

1) 50M students attend K-12 public schools.

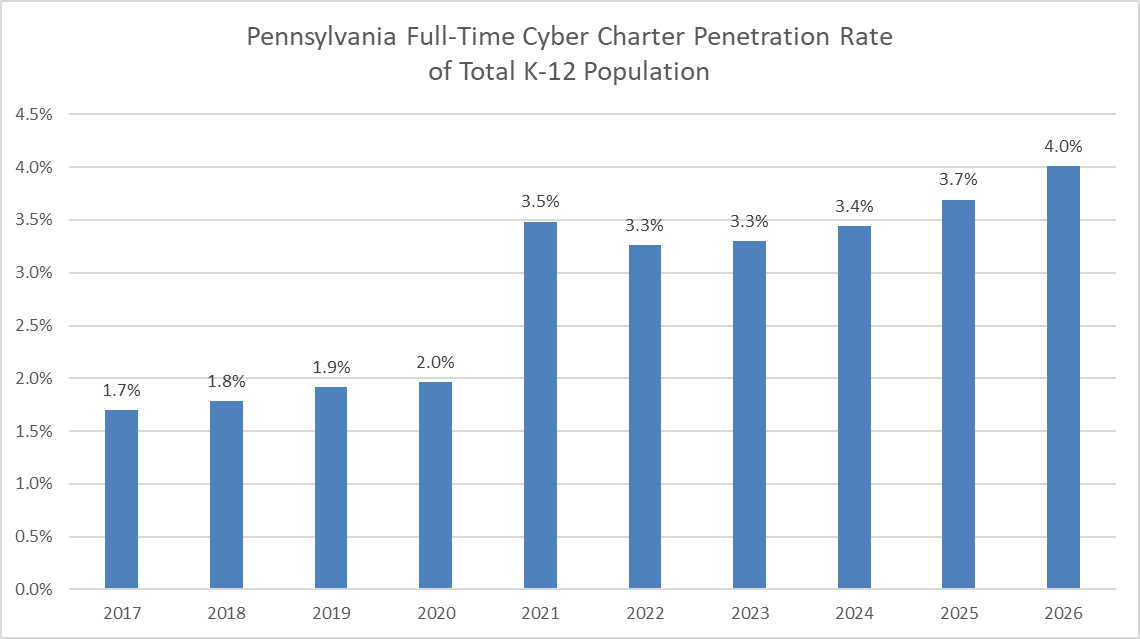

2) Cyber charter schools in Pennsylvania now enroll 4% of the state’s K–12 population. Pennsylvania lacks some of the structural barriers present in other states and allows statewide cyber charter operators to enroll students. Including district programs, whose data it not readily available publicly, the total virtual penetration rate might be closer to 5%.

3) Pennsylvania cyber charter enrollment growth continues to accelerate post-pandemic. Assuming a decelerating growth rate over the next five years, a 7% penetration rate in that state seems plausible. Applying this rate to the national 50M student count, that would imply 3.5M full-time virtual students.

4) Policy and regulatory resistance likely reduces the effective national penetration rate from 7% to 5%. Roughly 30% of U.S. K–12 students, or about 15M students, live in states with significant political, regulatory, union, or institutional opposition to large-scale statewide cyber charter expansion. If those students remain largely inaccessible, then 30% of the theoretical 3.5M-student opportunity, or 1.05M students, should be excluded from the addressable market. That leaves a regulatory-adjusted opportunity of approximately 2.45M students.

5) The current national market has enough room to grow roughly 3.5x–4.0x. A 2.45M-student addressable market compares with today’s estimated 600K–700K full-time virtual student base.

6) Assuming a 20-year period to penetrate the addressable market, the industry could see perhaps 7% annual enrollment growth. Cell phones achieved mass-market maturity in 25 years. Landline phones took 80 years. Full-time virtual charter schools launched in the late 90’s. This category will almost certainly mature more slowly than cell phones. Whether it matures faster than landline phones remains unclear.

The Addressable Market Assuming no Regulatory or Policy Constraints: 7%

Pennsylvania provides the cleanest benchmark for estimating the long-term addressable market for full-time virtual schooling in the United States.

As you can see from the chart below, today’s cyber charter penetration rate of 4% represents double the 2% rate found pre-pandemic in 2020.

Can the penetration rate once again double over the next twenty years? We can decompose that question in terms of supply/demand:

Supply - will the Pennsylvania governor/legislature seek to limit the offering as a greater % of students leave districts?

Demand - are there enough families that need this option?

No expert exists today who can categorically answer those questions. As Yogi Berra astutely observed “it’s tough to make predictions, especially about the future.”

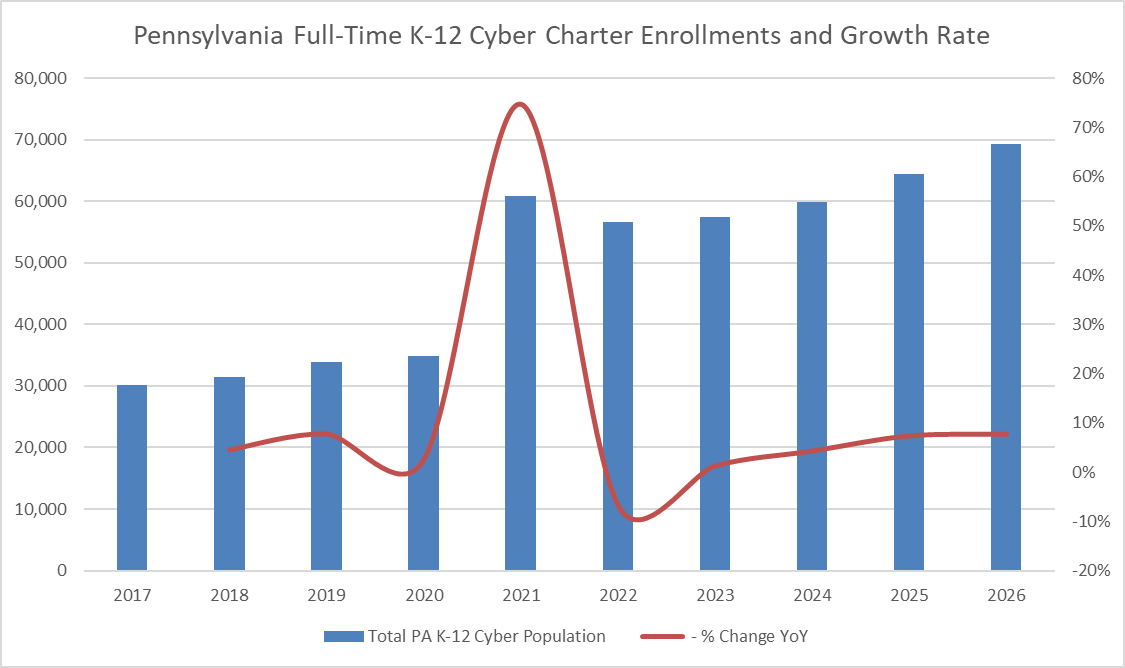

What gives me confidence on the likelihood of achieving this on the demand side is that Pennsylvania cyber charter enrollment growth continues to accelerate post-pandemic.

Acceleration implies that the flywheel is spinning faster. By flywheel I mean the self reinforcing loop where enrollments generate capital and awareness to drive further growth.

Parents continue shifting their kids into virtual options several years after schools reopened. From 2023 to 2026, enrollment grew from 57K to 69K students, a gain of nearly 12,000 students over three years.

My analysis assumes an analog of the Pennsylvania market to the national one. The reality is a bit more complicated.

Much of Pennsylvania’s cyber charter market concentration sits in one school. Commonwealth Charter Academy (CCA) enrolled close to 50% of the state’s cyber charter students. CCA has also expanded the definition of what a virtual school can offer families.

CCA has invested in physical and mobile infrastructure that has reduced core objections to virtual schooling: the lack of hands-on learning, socialization, and place-based student experience. The school operates Family Service Centers, mobile classrooms, AgWorks, and other experiential learning assets that bring parts of the physical school experience into a virtual model.

That infrastructure likely helped CCA enroll students who might otherwise have avoided the virtual school option.

Leaders at other virtual schools may seek to emulate CCA’s vision and execution. Or perhaps CCA serves as an outlier — Pennsylvania had unique funding characteristics (high funding per pupil) that allowed CCA to innovate.

Again there are fifty states, and each state’s circumstance is different. I could have reviewed another state with a high penetration rate.

The reason that I didn’t is that Pennsylvania has the cleanest data that can clearly tell the story. For example, Arizona appears to have one of the country’s highest online learning participation rates. But Arizona’s figure includes both part-time and full-time participation

Addressable Market Affected by Political and Regulatory Opposition

Some states will likely never fully support large-scale cyber charter expansion regardless of parent demand.

After full penetration of the addressable market we might see significant variability of rates in each US state like we see today.

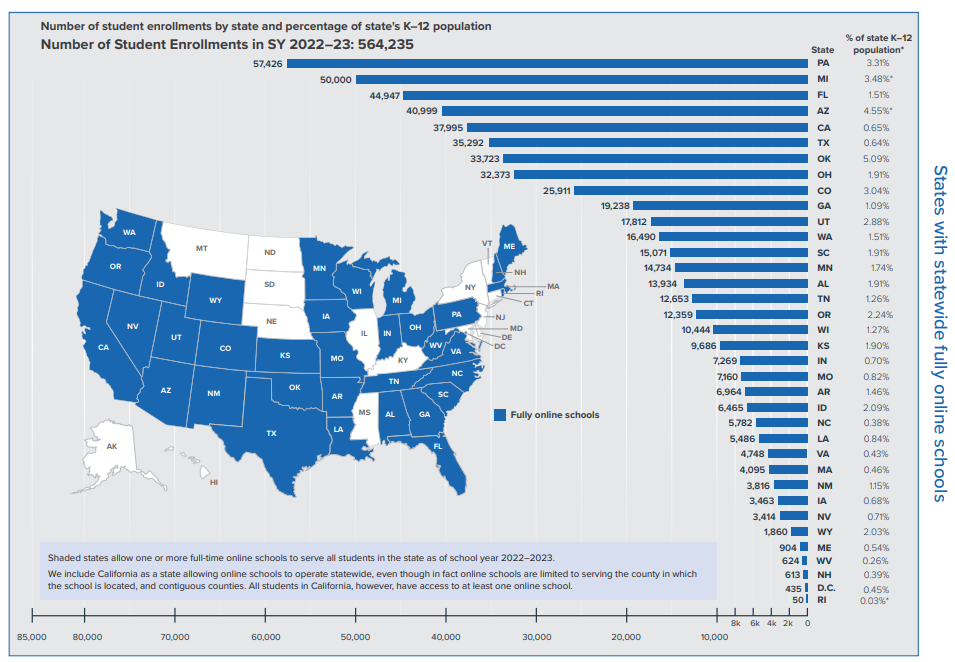

DLAC, the industry leader in virtual school conferences/meetings, provides helpful data on full-time virtual enrollment and penetration rates. In its latest report it has a chart (see below) that shows wide variation in virtual school enrollment by state as of 2022–23.

Approximately 30% of the US K–12 population resides in states with deep-rooted political, regulatory, union, and institutional opposition toward statewide virtual charter schools. These states include:

California

New York

Illinois

New Jersey

Washington

Massachusetts

Oregon

Connecticut

These states differ in their exact policies, but they generally constrain statewide cyber charter growth through restrictive authorization frameworks, district-centered virtual models, enrollment caps, moratoriums, funding constraints, or heightened oversight requirements.

California has one of the largest number of full-time virtual enrollments of any state, with close to 40K enrollments. However, this represents only 0.65% of the full-time K-12 population in the state.

More importantly, conditions do not appear favorable for material enrollment growth in California. The state once was an early leader in virtual school adoption. Now not so much.

California imposed a moratorium on new non-classroom-based charter schools from January 1, 2020 through January 1, 2026. That moratorium has now expired. In 2025, the legislature passed SB 414, which would have created a tighter oversight framework for non-classroom-based charter schools, but Governor Newsom vetoed the bill. Big picture, California’s policy trajectory doesn’t look especially encouraging for statewide virtual or cyber charter schools.

If we’re looking at over a twenty year period, it’s conceivable that things may change for the better in terms of parental choice in these states.

Explaining Supply Side Constraints, What Limits Rapid Adoption of the Virtual School Option

Debates over virtual schools often start with a disagreement over what success means. Operators and families may define success as solving a specific student problem, while critics often focus on standardized academic outcomes, mobility, and district funding effects.

As the former CEO of Pearson’s Connections Education used to say, ultimately virtual schools solve problems. The intent isn’t to replace the traditional classroom. Not to offer superior academic outcomes. It’s not even supposed to serve as a long-term solution for every family. It’s a highly specific offering for a family to solve a specific need at a specific time.

If a student uses virtual school for less than a year to navigate a crisis and then return to their local district, has the offering succeeded?

Critics of the offering are rightfully concerned that transitioning between traditional brick-and-mortar and virtual can cause students to fall behind academically.

I bring my own bias to this issue. As the parent of a neurodivergent child who struggles with the noise and sensory environment of a brick-and-mortar school, I understand the category differently than I did when I analyzed it professionally. Families seek virtual schooling because failures in the classroom are truly a family crisis. It’s a win to just get the child to the classroom on-time in the morning.

Here are the traditional concerns that sector critics provide.

Efficacy / outcomes / academic performance

Funding diversion from districts

Teacher staffing models

Public / private partnerships, where for-profit education management organizations manage schools

In March the North Carolina Charter Review Board approved four new remote academies. Democratic North Carolina Sen. Jay Chaudhuri used the words “education malpractice” to describe the expansion of virtual charter schools.

Democratic Rep. Rodney Pierce said that “I just think this is part of a bigger overall agenda to weaken public education.”

In 2023 the National Education Policy Center (NEPC) published their annual report on the sector but issued a press release with the title “Virtual Schools Continue to Underperform, Have Little Research Support, and Lack Adequate Regulation”

The Network for Public Education stated that “No. Online charter schools, also called cyber schools and virtual schools, are a poor choice for students almost every time. They’re mostly a way for for-profit education operators to cash in by exploiting the most vulnerable families in the public education system.”

During the Biden Administration, the Government Accountability Office issued a report titled “K-12 Education: Department of Education Should Help States Address Student Testing Issues and Financial Risks Associated with Virtual Schools, Particularly Virtual Charter Schools”

Tennessee’s 2023-24 Virtual Education Report suggested that there are credible academic reasons to limit expansion, alluding to higher student mobility, weaker achievement, lower growth scores

These reports may bring up good points. Meanwhile, in Maryland we lack access to virtual and hybrid school solutions that might serve as the best option for my child.

Interestingly, policy advocates haven’t issued a major report over the past three years, at least one that I’ve seen. For all I know a piece might come out tomorrow.

I wanted to engage with critics of the offering ahead of this piece so I could understand the objections that they have post-pandemic. I reached out to various authors of these reports, sending them a link to my prior Substack article. I received no replies back.

My sense is that we’re not going to see a broad national deregulatory wave anytime soon. It’s conceivable that we’ll see a selective loosening of legislative/regulatory pressures as a step function. Like we’re seeing with Texas today. That’s how this sector grew over the past twenty years. That also explains why virtual enrollment growth will likely continue at a steady, sub-double-digit pace rather than through a broad national surge (at least absent another pandemic).

Laggard states will presumably at some point accept that virtual schooling belongs in the public-school toolkit. Likely with rules to control quality, mandates on hiring union teachers, and limits on how a for-profit management company can contract with a school.

Florida: A Case Study in How a Regulatory Structure May Not Materially Benefit Stride or Pearson

Florida demonstrates that the growth in full-time virtual enrollments in a given state may not necessarily accrue to education management organizations like Stride, Pearson, or other full-time virtual school operators.

Each state has its own structure for how it permits, regulates, and distributes online instruction. Pennsylvania created a statewide cyber charter ecosystem dominated by independent operators. Florida took a different path.

Florida launched Florida Virtual School (FLVS) in 1997 to expand course access for rural and underserved students. In 2000, the legislature transformed FLVS into an independent statewide school district. In 2003, Florida codified a performance-based funding model in which FLVS receives funding only after students successfully complete courses.

Florida did not build a Pennsylvania-style cyber charter market where large statewide operators compete directly against local districts for enrollment. Instead, Florida built a district-centered virtual learning system.

Florida law requires districts to provide virtual instruction options. Districts can:

operate their own virtual programs,

partner with FLVS (using FLVS teachers and operational capabilities),

establish FLVS franchise programs (mostly FLVS courseware and tech systems),

or contract with approved providers (external entity provides courseware and manages operations).

As a result, Florida created one of the country’s largest virtual learning ecosystems without producing a Pennsylvania-style cyber charter market.

In Florida, districts remain central to the administration of the virtual school experience.

Families can:

remain enrolled in district schools while taking FLVS Flex courses (individual online course from FLVS without enrolling full-time in FLVS),

participate in district virtual instruction programs,

combine in-person and online schedules,

enroll full-time in FLVS,

or homeschool while relying heavily on FLVS coursework.

I estimate Florida’s effective virtual participation may already exceed 3%, although the state does not publish a clean figure that allows this to be measured precisely. Florida’s officially reported full-time virtual enrollment equals about 1.2% of statewide K–12 enrollment, but that figure excludes online instruction occurring through FLVS Flex, district channels, hybrid schedules, and homeschool pathways.

My estimate relies on FLVS disclosures showing that homeschool students represent 49% of the FLVS population (from the December 2025 “FLVS Home Education Guide”). Some of these students may function as de facto full-time virtual learners even though the state reports them under classifications tied to local districts rather than under full-time virtual enrollment categories.

Florida demonstrates that states can expand virtual learning substantially while still limiting the economic opportunity available to large independent virtual school operators.

Both Stride and Pearson operate within Florida. It’s just that the state’s own FLVS has substantial share that might otherwise have gone to Stride or Pearson.

Industry folks reading this piece might say that Florida is a unique circumstance driven by twenty years of policy, likely not to be replicated by other states. True, but all states have unique circumstances.

AI allows states to adopt the Florida model, as AI eliminates significant upfront costs for curriculum and technology development. There are a plethora of ex-Stride and Connections employees that can build out a FLVS for a state.

Laggard states with low virtual school penetration rates may follow the Pennsylvania model. They may follow the Florida model. They likely come up with another model. Which is to say, one cannot simply say that Stride and Connections have a 40% market share, and that as states allow this form of instruction Stride and Connections will maintain their market share. Maybe their market shares rises or maybe it falls with the addition of each new state.

Texas: The Largest Near-Term Growth Opportunity in Virtual Schools

Thus far, this piece has focused on the long-term size of the market. I’m adding this section because we may be witnessing a spike in virtual school enrollment in Texas given specific legislative changes. This will help test whether the addressable market remains more supply-constrained than demand-constrained.

Texas has 5.5M public K–12 students but only 60K full-time virtual enrollments, equal to a 1.1% penetration. So room exists between Texas and the Pennsylvania 4% cyber charter penetration rate. A Pennsylvania penetration rate of 4% would equal 220K full-time virtual students, more than triple the current enrollment level.

Historically, Texas constrained virtual enrollment through structural eligibility restrictions. Under the prior TXVSN framework, students needed to attend a Texas public school during the prior year in order to access full-time virtual programs. That rule blocked:

incoming kindergarten students,

students moving from out of state,

students transitioning from homeschool or private school environments.

Governor Abbott signed Senate Bill 569 into law in May 2025, restructuring Texas virtual education policy. The legislation loosens prior structural restrictions and gives districts and charter schools more flexibility to operate and expand virtual programs. It doesn’t create unlimited immediate expansion. New full-time virtual campuses still require authorization.

Senator Paul Bettencourt, the bill’s author, stated he expects virtual enrollment in Texas to double by the 2028–29 school year. This would imply roughly 120K virtual students by 2029.

Texas will serve as a test for real market demand for states that restricted this type of instruction.

Texas will also represent a major test of whether future virtual expansion benefits national education management organizations.

Conclusion

No one can predict the ultimate penetration rate of full-time virtual schooling with precision. Too many variables remain unknowable: policy choices, operator execution, academic outcomes, AI adoption, district responses, and parent preferences.

Still, the current national market appears small relative to states that allow this form of instruction.

This market isn’t akin to the adoption curve of technologies like mobile phones.

It’s also worth noting that the line between virtual and brick-and-mortar instruction may blur over time as districts integrate the following into traditional schools:

hybrid schedules

AI-supported instruction

asynchronous coursework

remote tutoring

flexible learning pathways

Political attitudes may also shift materially over the coming years. New research, operational successes/failures, student outcomes or cultural developments may either strengthen or weaken public support for virtual instruction. This may also affect public support for the education management organizations that operate virtual schools.

Like with other industries, AI may ultimately transform the category in ways that are difficult to comprehend today. AI-driven personalization, adaptive learning, tutoring and student support may improve the virtual learning experience. AI may also reduce barriers for districts and states seeking to build their own virtual infrastructure internally.

So here’s the range of outcomes as I see them.

Bull Case: Pennsylvania’s trajectory becomes the national model, and full-time virtual penetration ultimately approaches 7% in accessible states.

Base Case: Virtual schooling continues expanding, but policy resistance limits adoption in roughly 30% of the country. This produces a regulatory-adjusted national penetration rate closer to 5%.

Bear Case - High-profile efficacy studies, operational failures, fraud scandals, or political backlash trigger a regulatory pullback against virtual schools. States tighten enrollment caps, funding, authorizations, and accountability structures.

Whatever one thinks about policymakers, regulators, unions, or cyber charter operators with public company incentives, most participants in this debate genuinely believe they are acting in the best interests of students.

Virtual schools will not serve every student, and they don’t need to.

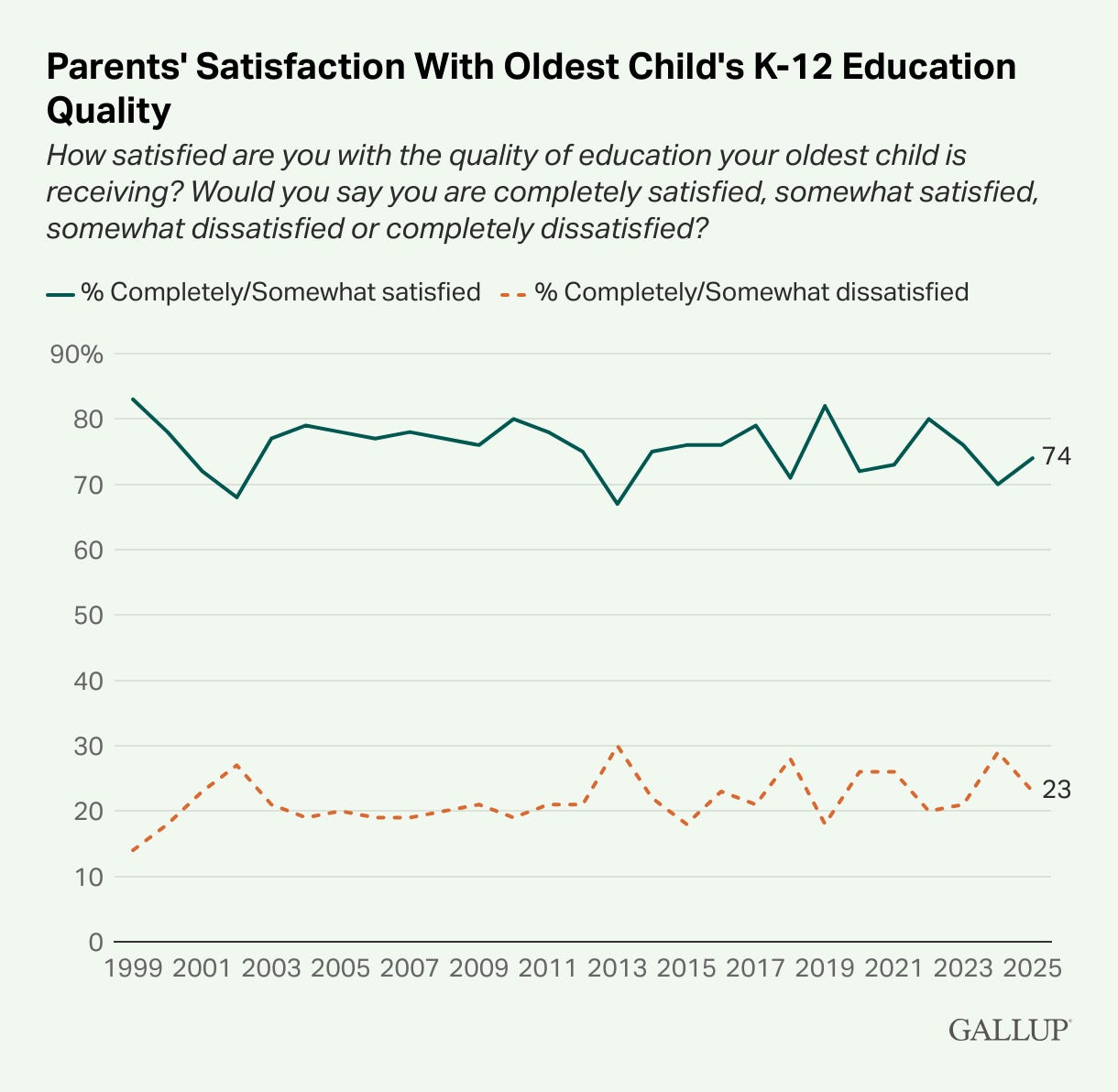

Gallup’s 2025 polling found that 23% of K–12 parents were either somewhat or completely dissatisfied with the education their oldest child receives. The pool of families experiencing dissatisfaction with their child’s current education is much larger than today’s full-time virtual enrollment base.

That’s a different way of sizing the potential market. If only a fraction of those dissatisfied families eventually choose full-time virtual schooling, the market can still grow several times larger than it is today.

Disclosure

At the time of this writing, I hold a position in Stride/K12 (LRN) stock. I reserve the right to buy or sell shares at any time, in any amount, and for any reason without prior notice or subsequent updates to the readers of this newsletter. This analysis is for informational purposes only and does not constitute professional investment advice.

FAQ

How large could the U.S. K-12 virtual school market ultimately become?

The full-time virtual school penetration could approach 7% of the U.S. K–12 population absent regulatory and political constraints. That would imply 3.5M full-time virtual students nationally. After excluding states with onerous rules, the more realistic long-term addressable market likely sits at a 5% penetration rate with 2.45M students, representing roughly 3.5x–4.0x the current market size.

Why can K-12 virtual school enrollments triple from current levels?

Cyber charter penetration in Pennsylvania already equals 4% of statewide K–12 enrollment, and enrollment growth continues accelerating even after schools reopened post-pandemic. That suggests virtual schooling has become an acceptable offering for families with specific needs.

Why does Pennsylvania serve as an analog for the broader US market?

Pennsylvania lacks many of the structural restrictions present in other states and allows statewide cyber charter operators to scale broadly. Because of that, Pennsylvania provides one of the best real-world benchmarks for estimating what mature virtual school penetration may look like nationally.

What appears to be the primary constraint on virtual school adoption today?

Political and regulatory resistance continues limiting expansion through enrollment caps, restrictive authorization frameworks, moratoriums, district-centered systems, and heightened oversight rules.

Why do some states continue resisting virtual school expansion?

Policymakers, unions, and education advocates remain concerned about academic outcomes, funding diversion from districts, teacher staffing models, student mobility, and the role of for-profit education management organizations. Several states continue imposing enrollment caps, restrictive authorization frameworks, moratoriums, district-centered models, and heightened oversight rules.

Which states are most resistant to statewide cyber charter expansion?

California, New York, Illinois, New Jersey, Washington, Massachusetts, Oregon, and Connecticut represent states with significant political, regulatory, union, or institutional opposition toward large-scale statewide cyber charter growth. Together, these states represent roughly 30% of the U.S. K–12 population.

Why is Florida important to understanding the future of virtual schooling?

Florida demonstrates that states can expand online learning substantially without necessarily benefiting operators like Stride or Pearson’s Connections Academy. The state built a district-centered virtual learning system around Florida Virtual School (FLVS) rather than a Pennsylvania-style statewide cyber charter market.

How does Florida’s virtual school system differ from Pennsylvania’s?

Florida built a district-centered virtual learning system around Florida Virtual School (FLVS) rather than a Pennsylvania-style statewide cyber charter market. Districts retain substantially more operational control in Florida through FLVS partnerships, FLVS franchise programs, district virtual instruction programs, and hybrid models.

Does Texas represent a large opportunity for increased virtual school enrollments over the coming years?

Texas represents the clearest near-term growth opportunity in the sector. The state has approximately 5.5 million public K–12 students but only about 60,000 full-time virtual enrollments, equivalent to roughly 1.1% penetration.

What changed recently in Texas virtual school policy?

Texas passed Senate Bill 569 in 2025, loosening structural restrictions that historically constrained virtual enrollment growth. Prior rules required students to attend a Texas public school during the prior year before accessing full-time virtual programs.

How large are Stride and Pearson within the current market?

Stride and Pearson may collectively serve 40%–50% of the existing full-time virtual school market, depending on definitions. Stride currently serves roughly 250,000 virtual school enrollments. Pearson’s Connections Academy reportedly served roughly 100,000 students as of two years ago.

Why might AI improve virtual schooling over time?

AI may improve personalized instruction, tutoring, adaptive learning, asynchronous coursework, and student support systems. AI may also reduce barriers for districts and states seeking to build their own virtual infrastructure internally.

Could the distinction between virtual schools and traditional schools blur over time?

Yes. Over time, districts may increasingly integrate hybrid schedules, AI-supported instruction, asynchronous coursework, remote tutoring, and flexible learning pathways into traditional schools. The future may look less binary than today’s distinction between virtual and brick-and-mortar education.

What is the biggest long-term risk to the virtual school market?

The largest risk remains political and regulatory backlash. Negative efficacy studies, operational failures, fraud scandals, or broader political opposition could trigger tighter enrollment caps, funding restrictions, authorization rules, and accountability structures.