Stride (LRN), Customer Efficacy Risk, and Investor Diligence in the AI Era

The announced closure of a large Texas customer has investors concerned. While always possible, it's highly unlikely IMHO another large school will close in the near-term due to efficacy issues.

In this piece I’m addressing the question readers asked me after the announced closure of Lone Star Online Academy in Texas: could Stride lose another large school due to efficacy concerns? The issue was raised following the recently announced closure of Lone Star Online Academy (LSOA) in Texas. Big picture, while anything can always happen, I don’t see another large school closing over the near term due to efficacy. To be clear, there are Stride powered schools with weak academic profiles that deserve monitoring. There are schools where state accountability results aren’t great. But I don’t see another large Stride school with the same combination of size, repeated failing ratings, and a visible near-term closure catalyst like LSOA.

That doesn’t mean there’s no risk. There’s always school closure risk in this business. Charters get non-renewed. District partners change course. State accountability systems change. Authorizers act.

But a weak school rating isn’t the same thing as a near-term revenue loss.

A school’s rating has to intersect with a real mechanism/process for closure: a turnaround plan, a renewal vote, a state intervention process, a rejected improvement plan, or a district decision to stop hosting the school.

I continue to own Stride LRN stock post-LSOA closure despite evident risks. As Captain Kirk said, risk is our business. The job of the investment professional is to weigh risk relative to upside. The virtual school market continues to grow at a meaningful pace, driven by post-pandemic tailwinds. Sometimes it’s a bumpy ride.

Yesterday I published a Substack note on the apparent shutdown of Lone Star Online Academy (LSOA) in Texas. I assumed that the closure was related to efficacy, with LSOA receiving a F rating by the Texas Education Agency (TEA) for several consecutive years now.

The piece ended up being one of the more widely read things I’ve published.

After I posted the article on LinkedIn, a number of investment professionals at institutional shops reached out. They wanted to understand what happened with Lone Star, whether it could happen again at another Stride school, and whether they should sell the stock. Thus this follow up piece.

The reaction was fascinating to me because it highlighted something that makes Stride such an interesting company to analyze. Investors can own the stock, understand the financial model, and articulate why the stock represents an attractive opportunity. And yet, many investors don’t fully understand the school business and the risks that exist.

Stride isn’t a simple SaaS-like education platform where revenue renews unless customers churn. This is a public-school operating model tied to state accountability systems, district partners, charter authorizers, renewal cycles, political pressure, and student outcomes.

Most of the information needed to analyze the company’s risk is public. State report cards. Enrollment data. Accountability frameworks. School board materials. The problem is that the work to understand this company and its risk can at times be tedious.

One can get lost in the voluminous amount of information. I did twenty years ago while on the sell-side. I saw politicians making claims about school closures and funding cuts, and wrote notes expressing concern about Stride, then known as K12. I didn’t understand then that one has to take public information with a grain of salt, and discern when truly real risk exists. Painful lesson for myself and more importantly for the folks at the company who had to deal with a sell-side analyst writing notes about how the sky was always falling.

Before I explain why I think the risk of other large closures based on efficacy is limited at this time, it’s important to explain the challenge with consuming efficacy information regarding schools in the context of state accountability frameworks.

The Problem With Analyzing Virtual School Efficacy with State Accountability Frameworks

Virtual schools exist because of the deficiencies of the traditional school system in serving non-traditional students.

Families don’t choose a statewide virtual school because everything is going perfectly in their local school. The students that enroll are academically behind, anxious, bullied, medically fragile, etc… Yes, investors understand this part.

What apparently some investors don’t get – the population served by these schools can make the schools look terrible under state accountability frameworks. The frameworks often don’t fully account for student mobility, prior academic performance, credit deficiency, mental health issues, or why the student moved to virtual school in the first place. At LSOA 86% of the student population is economically disadvantaged. Does that have a role to play in a school’s efficacy? Probably.

In an ideal world state accountability frameworks would exist focused on the type of population that enrolls at virtual school. In an ideal world students would have personalized instruction in the traditional classroom rather than the cookie cutter factory assembly line instruction that Pink Floyd mocked in The Wall. Unfortunately a clear and evident disconnect exists between ideal and reality.

The private sector steps into the education market when the traditional public system fails students. Then the private sector gets attacked because the outcomes aren’t pristine.

Investors may have views on the morality of the debate, but the investment question is narrower: can more revenue disappear because schools close or contracts aren’t renewed? The frameworks exist, it isn’t particularly constructive to debate whether the frameworks are fair.

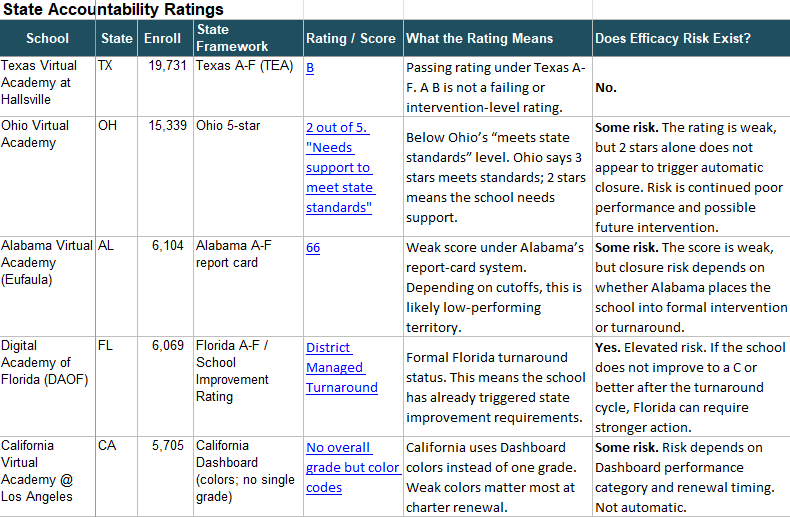

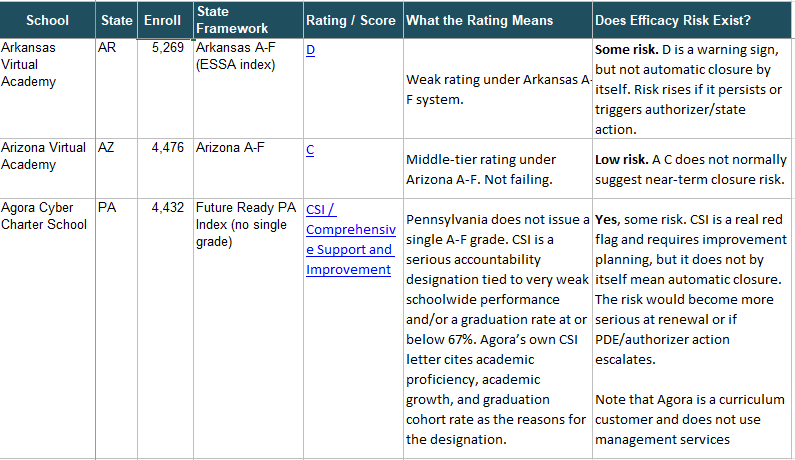

Does Stride Have Other Large Schools At Risk from Closure Due to Efficacy? I Don’t See It

I simply don’t see an obvious second Lone Star type closure among large Stride powered schools based on current public information. I see schools with troubling academic profiles and weak outcomes. But I don’t see another large Stride school with the same combination of size, poor ratings, and visible near-term closure catalyst.

Thanks to AI, it’s easier than ever for investors to pull basic information about schools. That said, this exercise still required multiple iterations because AI can produce incorrect data and misinterpret state accountability systems.

In the table below, the final column addresses whether efficacy risk exists. That’s different from saying a school is likely to close. Important distinction.

Big picture, the largest Stride customer, Texas Virtual Academy at Hallsville, has a passing Texas rating.

The other schools have various efficacy challenges. As one would expect from schools serving this type of student population.

Ohio Virtual Academy has a two star rating in a state where three stars meets state standards. So obviously that’s not great, but there is quite a distance between being below meeting state standards and closure.

Digital Academy of Florida is one of the more important watch-list names because it appears to be under a “District Managed Turnaround”, a formal Florida improvement process. That doesn’t mean the school is closing, but it does mean the state has moved the school into a more serious accountability framework. I found a turnaround plan online, but it’s dated to 2024 so no idea if it’s the latest and greatest.

Agora Cyber Charter school, just a curriculum customer and not a managed school, is listed as a comprehensive support and improvement (CSI) school. That’s obviously not good. A CSI designation is a label assigned to schools that fall into the lowest 5% of Title I performers or have low graduation rates, triggering increased federal scrutiny and mandatory improvement plans.

While these schools aren’t obvious near-term closure candidates, investors should probably continue to monitor them to assess risk.

Here’s the thing, Stride has significantly scaled to the point where it can weather the loss of a customer and still see revenue growth. Stride lost Insight in Pennsylvania last year and no one noticed because of the growth elsewhere in the overall portfolio.

What made Lone Star different

Lone Star was the obvious candidate for a large school closure because it had several years of failing ratings. What was unusual wasn’t that a poorly rated school faced consequences. Rather, how abruptly the situation changed.

School closures are usually more telegraphed. There are school board meetings, staff reports, local articles, parent campaigns, and public debate. Families fight to keep schools open. Politicians get involved. Local reporters write stories.

This case appeared to catch everyone off guard. School employees and families. At least based off of social media posts.

The data was public. The ratings were public. The enrollment size was public. That being said, the apparent speed of the closure was unusual, which helps explain why investors were caught off guard.

Back in 2017 Stride’s Hoosier Academies Virtual School shut down due to efficacy issues. As a consequence of the efficacy issues, the board voted not to renew its charter. There were leading indicators of when it happened. The school had six straight Fs on the state accountability metrics. There were discussions. And this for a smaller school than LSOA.

Efficacy Risk From Here

It’s conceivable that Stride can find homes for the Lone Star families seeking options for their students. Revenue for Stride may not materially be impacted.

The bigger efficacy risk for investors is the narrative cycle that Lone Star could create.

An enterprising short seller could decide to make a public case that Stride has significant revenue at risk because of other efficacy concerns. A reporter could write about Lone Star and then broaden the story into a critique of virtual schools. That could increase political scrutiny, hurt supply expansion, and pressure valuation multiples for both Stride and Pearson.

That may sound like conspiracy thinking. For those who covered education stocks 2008-2011, we saw that reality unfold when the for-profit education sector was under attack. It wasn’t particularly pleasant.

That doesn’t mean the bear case is right and/or will happen. It does mean investors need to understand what they own.

Stride operates in a complicated part of the education market. The company benefits from demand created by failures in the traditional system, but it’s also exposed to public accountability frameworks that may not fully account for the population these schools serve.

This is also why Stride and Pearson have developed such strong positions in the virtual school market. Execution is hard. Threading the needle between enrollment growth, family demand, state accountability, authorizer relationships, political scrutiny, and student outcomes is difficult.

You can argue that these risks justify a lower valuation multiple. You can also argue that the complexity of the model is part of the moat which results in an increased valuation multiple. The valuation multiple declined over the past year due to a challenged learning management system implementation. I continue to believe that the multiple should expand again once the company anniversaries the last enrollment cycle. Obviously this customer loss makes the multiple recovery a bit more difficult.

Lessons for Investors

This is a company where some of the most important risks aren’t obvious from the 10-K. They’re in state accountability systems, charter renewal calendars, district relationships, and school-level performance data.

In the AI era, this kind of diligence is much easier to do than it used to be. Investors shouldn’t have been surprised that Lone Star had efficacy risk, even if the apparent speed of the closure was surprising.

What Investors Should Ask Management

One thing that’s been missing from Stride conference calls is a serious discussion of efficacy.

For several years, the company benefited from powerful market tailwinds. The addressable market expanded. Enrollment demand was strong. The category was growing. The investor conversation focused on revenue growth, margin expansion, career learning, etc…

Over the past year, the conversation shifted somewhat because of the learning management system challenges. That was front and center.

But after Lone Star, I think investors will start to ask a more basic set of questions about school efficacy. Not just “what happened at Lone Star?” The school had three Fs in a row. The more important question is why the school had three Fs in a row and what Stride could have done differently, if anything.

For those of you invested in the stock, here’s what I would recommend you ask:

When a Stride-supported school receives weak state accountability ratings, what exactly does Stride do? Is there a formal internal playbook for underperforming schools?

Why did Lone Star receive three consecutive F ratings? Was that primarily a function of student inputs? Was it a school leadership issue?

What could Stride have done differently at Lone Star? Were there additional resources, staffing changes, student-support interventions, tutoring programs, teacher supports, attendance initiatives, or academic policies that could have improved outcomes?

Is there any demonstrable improvement at other managed schools when allocated additional resources? Resources that may require an investment in margin?

Are there enrollment policies that could improve more favorable academic outcomes? For example, should certain schools limit mid-year enrollment, change start-date policies, strengthen onboarding, or set clearer expectations for families before enrollment?

How is AI changing the efficacy equation?

What evidence can management provide that Stride improves outcomes for the students it serves? Not marketing language. Actual evidence. Cohort growth, graduation improvement, credit recovery, course completion, persistence, or outcomes adjusted for incoming student profile.

The question investors should be asking is not simply whether another school can close. Of course another school can close. This is public education. There will always be school churn. This is a really hard business to do, and Stride does it better than anyone else in its category.

The better question is whether Stride has a rigorous, repeatable model for identifying weak academic outcomes early, allocating resources to schools that need help, improving student performance, and reducing the risk that efficacy issues become authorizer, political, or revenue events.

These are the questions that investors should ask on the next earnings call.

Disclosure: I am a shareholder of Stride, Inc. This article reflects my personal views and is not investment advice. I may buy, sell, or otherwise change my position in Stride at any time without notice. I have no business relationship with Stride, Pearson, or any of the schools discussed in this piece. The analysis is based on publicly available information, including state accountability data, school report cards, school websites, and related public documents. While I’ve tried to be accurate, state accountability systems are complicated, school-level data can change, and some facts may be incomplete or subject to interpretation. Readers should do their own work and not rely on this article as the basis for any investment decision.