Skillsoft, the sale of Global Knowledge, and the SPAC-Era Quest for Scale

A SPAC-era platform story and the enduring cost of buying scale

Skillsoft is a case study in how 2020s SPAC-era incentives pushed companies toward poor capital allocation decisions. The recently announced sale of Global Knowledge closes that chapter in the company’s story. The question is whether a simplified company with a large debt burden can find a path forward. AI complicates the story further.

This piece isn’t about whether investors should buy Skillsoft stock.

Rather, it’s about what Skillsoft reveals about the SPAC (special purpose acquisition company) market then and now.

In conversations with management teams over the past year, I’ve learned that SPAC has become a dirty word. That’s understandable given how many 2020–2021 SPACs performed.

I’m writing this to explain two things: first, how the SPAC process helped push a real company with real revenue into a difficult situation from which it is only now trying to recover; and second, why the lessons from that period have made today’s SPAC market more disciplined than it was before.

The timing of this piece is relevant because Skillsoft reported its 1QF27 results last night, with management emphasizing that following the sale of Global Knowledge the company’s balance sheet is now its central focus.

Skillsoft (NYSE: SKIL), an edtech provider that primarily sells learning and talent development solutions to enterprises, announced on May 20th that it intends to sell a subsidiary called Global Knowledge to a private equity entity.

Normally, a small divestiture for a company with a $55M market capitalization wouldn’t warrant a note like this. Companies buy and sell assets all the time.

It’s not the sale itself that’s interesting.

Rather, it’s the circumstances around how Skillsoft went public with a $1.5B enterprise value, how Global Knowledge became part of the Skillsoft story, and how capital market incentives can push companies toward M&A decisions that make sense in theory but later create long-lasting problems for the business.

Deals like this one explain how the SPAC market contracted and evolved into something better.

Skillsoft went public through a deSPAC transaction in 2021. A SPAC raises capital in an IPO with the intent to later merge with a private company and take that company public. Remember that the early 2020s market was awash in liquidity thanks to the pandemic, the Federal Reserve response, and federal government action. Sponsors used this opportunity to take companies public, particularly those companies that didn’t have the profitability or financial statement optics that would work through a traditional IPO process.

Unfortunately for shareholders, most SPACs from that period performed poorly.

Many of those who went through the SPAC process didn’t generate meaningful revenue or EBITDA. Many first-wave SPACs were tied to speculative next-generation categories, including electric vehicles, space, fintech, and other long-duration growth stories. Every era of technological revolution includes speculation, and the early 2020s was no exception. The speculation was obvious at the time. Case in point, see this Business Insider article about how “experts warn they’re creating the next dot-com bubble” regarding EVs.

Skillsoft was different. It had revenue, customers, and cash flow. I used to cover the company as an analyst on the sell-side twenty years ago before it was acquired by private equity. Good cash flow generating company with a good recurring revenue business model, but suffered from anemic revenue growth.

Unfortunately, the private equity owners who took the company private saddled Skillsoft with an unsustainable debt level.

As a consequence of the high debt load Skillsoft underwent Chapter 11 in 2020. The lenders saw their debt converted to equity. As most lenders are not in the business of owning equity they naturally wanted to exit their position. The bankruptcy process reduced Skillsoft’s debt dramatically, but it still had meaningful leverage. A company with lackluster organic revenue growth and a post-bankruptcy balance sheet with debt may not have represented an easy IPO candidate.

Meanwhile, SPAC IPOs were taking off.

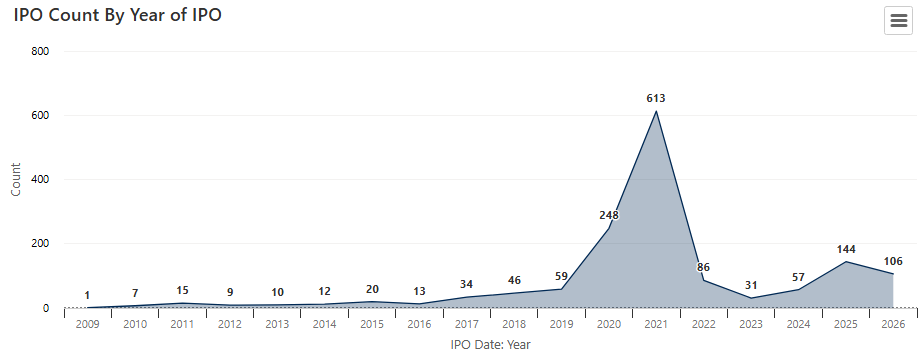

There were 59 SPAC IPOs in 2019.

248 in 2020.

613 in 2021.

A larger company with a broader enterprise platform presumably represented a better story to institutional investors to go public via a SPAC merger.

That context helps explain the Global Knowledge acquisition.

Combining Skillsoft with Global Knowledge in theory created the sort of story institutional investors could accept. The largest player in enterprise instructor-led training, Global Knowledge brought to Skillsoft customer relationships for cross-sell opportunities, cost synergies, and most importantly a more complete corporate learning platform story.

Skillsoft acquired Global Knowledge for close to $230M in 2021. Today, Skillsoft is selling Global Knowledge for a headline basis of roughly $18M. But that amount overstates the economics of the recently announced transaction. Rather, the transaction is tied to Global Knowledge’s own cash, future cash flow generation, a seller note, and collectability risk.

The mismatch between Skillsoft and Global Knowledge and the challenges with the Global Knowledge were fairly evident to edtech investors, or really any investor. That may explain why over 50% of SPAC investors sought redemptions before the deSPAC merger went through. One of the beauties of the SPAC business model is that investors can pursue redemptions before the business combination vote between the SPAC and target company.

Here’s what SPAC investors may have seen.

Skillsoft had a great subscription revenue model that provided a high level of visibility. Enterprises paid for access to Skillsoft’s content and platform. The natural acquisition fit for Skillsoft was tuck-in acquisitions that focused on the core corporate learning category with recurring revenue models. Preferably a company that had cash or generated meaningful free cash flow that could help Skillsoft delever.

Global Knowledge was not that.

Global Knowledge was an instructor-led IT training business. The company provided training tied to technology certifications and vendor ecosystems. Think Cisco, Microsoft, AWS, and other technical training categories. A customer buying seats for a scheduled course isn’t subscription, it’s transaction-oriented with lumpier revenue.

The whole point of Skillsoft’s public-company story should’ve been the quality of the revenue with recurring revenue characteristics.

Beyond the type of revenue, it was clear that the pandemic was accelerating trends on how employees consumed learning. Employers were gaining comfort with remote learning and self-paced instruction. Long-term value was moving toward scalable content, flexible learning pathways, and subscription access. Think Coursera and Udemy.

Global Knowledge made Skillsoft bigger but the model worse. It added a declining, delivery-heavy training business to a company that should’ve been trying to convince investors it had a recurring-revenue enterprise learning platform.

Skillsoft and Global Knowledge merged with its sponsor SPAC in 2021. Since then, shares have declined by over 95%.

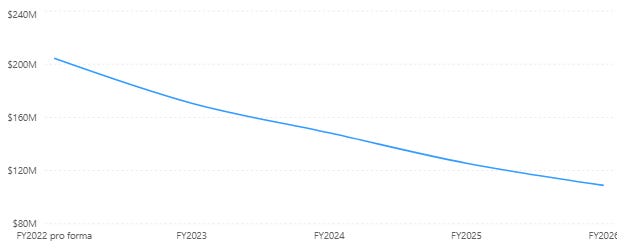

Global Knowledge revenue declined from ~$200M on a FY2022 pro forma basis to close to $100M in FY2026.

Then Skillsoft made things worse.

It acquired Codecademy in 2022 for $525M, financed by equity and debt.

Codecademy was an online interactive coding education platform. It taught users programming, data, cloud, cybersecurity, web development, AI, and related technical skills through self-paced interactive lessons and hands-on practice.

The problems with this 2022 acquisition, obvious at that time:

Codecademy was primarily a consumer play, a problem given that Skillsoft sold to enterprises. Skillsoft didn’t buy a proven enterprise learning business. It bought a consumer-origin coding platform and hoped its enterprise distribution could convert it into an enterprise growth engine.

SKIL financed the acquisition with debt. Skillsoft already had a levered balance sheet. The acquisition resulted in Skillsoft adding another $160M of debt.

The purchase price was simply too high, as Skillsoft bought at peak valuation multiples for edtech companies. Skillsoft bought Codecademy for $525M while at the time Codecademy was expected to generate only $42M of revenue. That’s more than 12x revenue for a small business not yet profitable. Skillsoft disclosed that Codecademy was expected to generate negative $20M of EBITDA in 2021.

An enterprise company buying a consumer company with a peak multiple while taking on debt is an interesting choice. Definitely a high risk capital allocation decision.

What we didn’t know then was how quickly the market would turn against entry-level coding education, or how AI would change the perceived value of beginner coding instruction.

How the SPAC Market Has Improved Since

There were 613 SPAC IPOs in 2021.

By 2023, there were only 31.

The market has rebounded a bit over the past two years with 144 SPAC IPOs in 2025.

SPACs can provide great value.

They can help a private company access public capital faster than a traditional IPO. It can allow investors to participate in a company earlier than they otherwise might. It can give a management team an alternative path to liquidity. It can create a vehicle for experienced sponsors to identify private companies that would benefit from being public.

The issue is that the early 2020s SPAC version operated in an environment that allowed for and at times encouraged bad behavior.

The market was awash in liquidity. Interest rates were low. Sponsors needed targets. Investors were willing to invest in companies with large projections about the future.

The market back then rewarded SPACs with scale that were well positioned to penetrate a large addressable market.

That boom created an incentive to package companies for the public markets.

In the case of Skillsoft, the traditional IPO wasn’t realistic. Skillsoft had just come out of bankruptcy, had limited growth, and carried leverage. That’s likely why the SPAC route was appealing. That also may explain the need to package Skillsoft with Global Knowledge as a larger platform.

Apparently only about one in five companies that went public via SPAC in 2020 and 2021 were later trading above the standard $10 SPAC IPO price.

Perhaps this explains why in conversations over the past year with management teams I’ve learned that SPACs are viewed unfavorably by some.

SPACs failed in the early 2020s because:

too much capital chased too few good targets

sponsors were incentivized to complete a transaction

companies used projections that wouldn’t have worked in a normal IPO. SPACs allowed companies to market long-term forecasts more aggressively.

Skillsoft is the cautionary example.

That’s why Skillsoft is a useful case study. The company wasn’t a fraud. It wasn’t pre-revenue. It wasn’t a concept stock. It was a real business that entered the public markets with too much debt and a strategy that depended on acquired scale holding up. When Global Knowledge declined and Codecademy didn’t grow per expectations but added debt, the company struggled.

There’s evidence that the SPAC market has become more disciplined since the first-wave SPAC boom. That discipline is coming from regulation, investor skepticism, a smaller SPAC IPO market, more experienced sponsors, and tougher scrutiny of projections, dilution, and sponsor economics.

In 2024, the SEC adopted new SPAC rules requiring enhanced disclosure around conflicts of interest, sponsor compensation, dilution, projections, and target company information in deSPAC transactions. The point was to move SPAC disclosure closer to IPO-style investor protection.

SPACs can be a useful capital markets tool when the target is mature enough, the balance sheet is appropriate, the valuation is reasonable, the sponsor is credible, and the post-close company has enough cash to execute its plan.

Where Does Skillsoft Go From Here?

The Global Knowledge sale simplifies Skillsoft.

Unfortunately, it doesn’t fix Skillsoft’s problems.

Skillsoft has three challenges.

First, debt.

The company has close to $570M of debt versus $115M in cash. That represents net debt to EBITDA of more than 4x. Most of Skillsoft’s free cash flow goes to interest payments, which leaves little cash to reinvest in the company’s platform. S&P’s latest outlook for the company has a B- rating.

Second, revenue decline.

The company reported results last night including a 5% YoY decline in 1Q27. It’s unclear whether management can stabilize the business let alone drive revenue growth.

Third, AI may alter how enterprises view corporate learning platforms.

Generative AI has commoditized content. What that means for platforms like Skillsoft remains unclear. AI could hurt the perceived value of traditional learning content. It could also strengthen the need for enterprise platforms that help companies map skills, train employees, assess capabilities, and manage compliance at scale.

Skillsoft clearly needs to lower its debt. The company needs to reduce cash interest expense. It needs a balance sheet that provides the core business flexibility.

If Skillsoft can recapitalize, the story becomes much more interesting.

The company could use the remaining platform to consolidate smaller enterprise learning and skills companies.

The obvious problem with that comment is that the company’s track record on acquisitions isn’t great.

That being said, there is a new management team in place.

The core business has value. It has enterprise customers. It has recurring revenue. It has adjusted EBITDA. It would have free cash flow if it didn’t have to service debt.

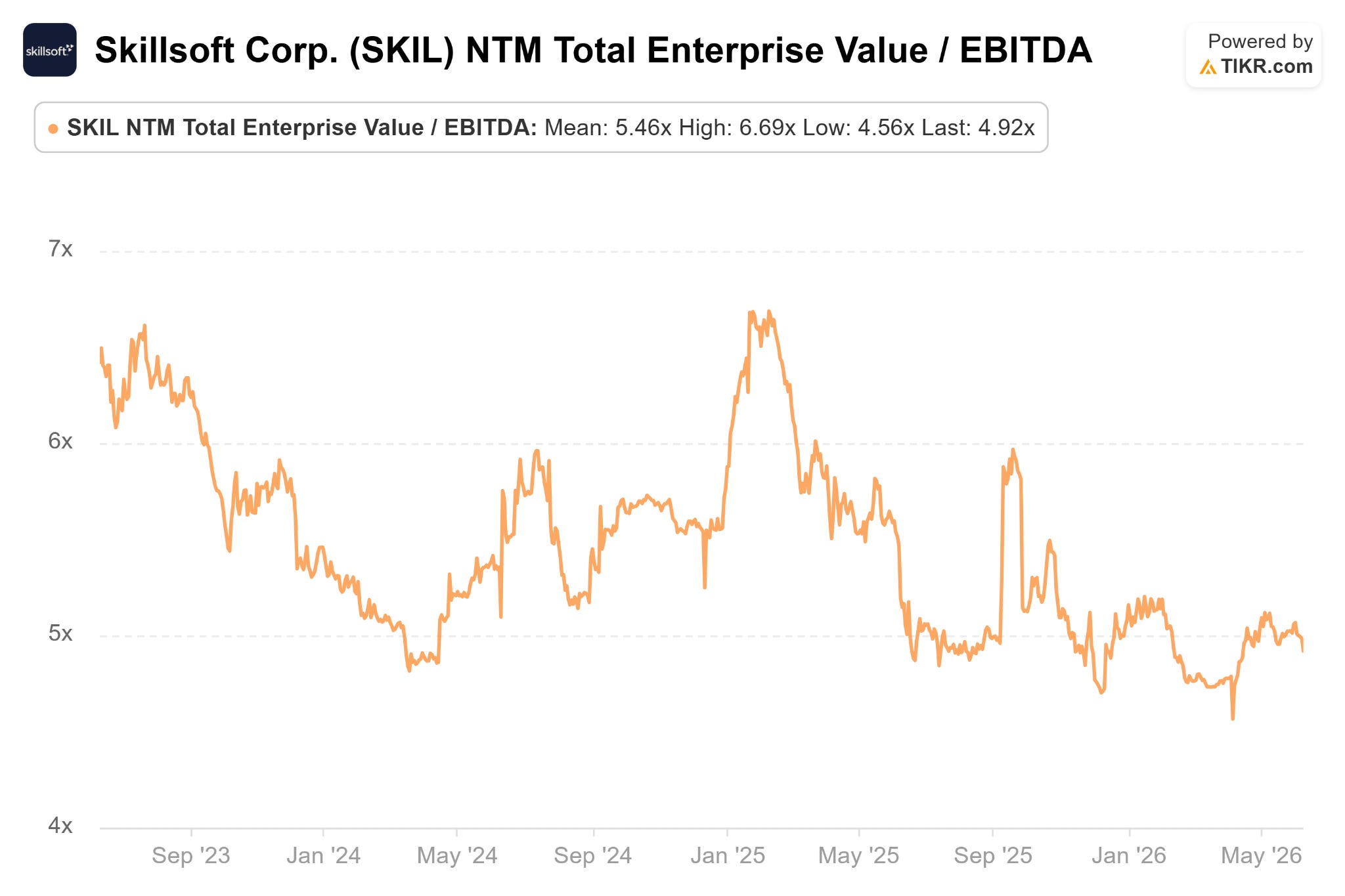

As you can see from the chart below, Skillsoft’s valuation multiple has compressed from over 6x EV/EBITDA to now about 5x. Note that Coursera and Udemy compressed all the way to 2-3x EV/EBITDA given investor concerns regarding AI substitution.

So is this a buy?

Not for me. At least not yet.

When the company reported results last night, comments regarding execution were encouraging.

Dollar retention rate of 105% (better than 100% is good, certainly better than Coursera)

Higher YoY bookings

Expanding pipeline

An increase in average deal size

But unfortunately the balance sheet simply has too much debt and pays too much in interest expense to service that debt.

To be clear, the current management team understands this and has focused on the right things.

Management suggested that following the sale of Global Knowledge, refinancing the debt will be management’s top priority.

This is what the CEO said on the call last night:

Once the GK divestiture is complete, addressing our upcoming debt maturities will be management’s top financial priority. We recognize this is important to all of our stakeholders. We will evaluate all alternatives with discipline and urgency. The actions we are taking to simplify the company, improve leverage and strengthen free cash flow visibility are all designed to give us maximum flexibility as we approach that work.

I hope that management can initiate a recap in some way. Having lower debt would allow the company to invest in its current offering given the opportunities and threats that AI poses. It would also open the door for accretive tuck-in acquisitions that would complement the existing business.

Unfortunately, Skillsoft still suffers from legacy baggage from its deSPAC process. In a different reality with a different set of capital allocation decisions Skillsoft’s enterprise value would reflect mostly equity rather than debt.

Skillsoft may still become the enterprise learning platform it should have been all along.

Disclosure: This article reflects my personal views and is for informational and educational purposes only. It is not investment advice, a recommendation to buy or sell any security, or a solicitation to engage in any investment transaction. I do not currently own shares of Skillsoft. I may, however, buy or sell securities discussed in this article in the future without updating this disclosure. The analysis is based on publicly available information, company filings, earnings materials, press releases, and my own interpretation of those materials. I may be wrong, and readers should do their own work and consult their own financial, legal, tax, or investment advisors before making any investment decision.