EdTech Q1 Review: AI May Drive the Narrative, But Fundamentals Still Drive Relative Valuation

While AI is shaping investor expectations with sector re-ratings, relative valuation across edtech and education stocks remains firmly tied to financial performance

TL;DR

While AI may be driving sector re-ratings, valuation in edtech still holds on a relative basis

Across edtech, relative valuation is anchored in fundamentals - primarily revenue growth, not irrational AI narratives

Coursera (COUR) at ~3x EV/EBITDA looks distressed, but on a relative basis with current consensus estimates, it’s trading exactly in-line with its peers. And if/when the merger with Udemy (UDMY) goes through, the stock could see valuation multiple expansion if the regression model holds

Duolingo (DUOL) stock may have declined by 78% from peak, but on a relative valuation basis it’s trading where it should relative to peers

Although Stride (LRN) lacks a clean comp set, when anchored to postsecondary peers, it appears as undervalued with clear multiple expansion potential

Postsecondary stocks have split into three distinct buckets:

vocational (premium valuation), healthcare/ground campus (mid-tier valuation), and online (discounted valuation)Bottom line: AI hasn’t changed the rules of valuation—fundamentals still determine where stocks trade

Has AI Changed How Publicly Traded Edtech Companies Are Valued?

HBO commentator Larry Merchant famously said during the Mike Tyson - Buster Douglas fight, Douglas is asking of Tyson some questions he hasn’t been asked before

Douglas, at that point, was doing the unthinkable—breaking a model everyone assumed was untouchable.

We’re seeing something similar in the world of edtech given AI disruption.

We assume a company will exist because it already has. That’s what’s called normalcy bias. That’s when people believe things will continue functioning as they always have and ignore impending disasters. Investors already played that game with Chegg and got burned, with the stock losing close to 99% of its value. That business collapsed over the span of two years given AI substitution of its core product.

In edtech, basic questions are no longer theoretical:

How will people actually learn?

What is the value of a credential or degree in a world where content is free?

Why subscribe to a content platform when AI can generate answers on demand?

Which job categories are truly insulated from AI substitution?

For investors, the more immediate question is simpler:

How do you even value these businesses?

In this post Q1 write-up, I’m focusing on whether edtech relative valuation has merit.

Relative valuation determines how a company is priced in relation to its peers, typically using multiples such as EV/EBITDA. It is, in practice, how the public markets price assets.

With AI driving volatility across digital and edtech names in recent months, it’s reasonable to ask whether valuations still make sense.

Take Coursera as an example. The stock trades at roughly ~3x EV/NTM EBITDA, a level that typically implies structural decline. Yet the business is still growing, and to date has not seen revenue materially impacted by AI.

So what explains Coursera’s valuation multiple?

Why is it trading below the valuation of postsecondary companies?

Is the market even pricing companies relative to peers?

And if so, what drives differences in valuation across the group?

Approach and Findings

To answer these questions, I constructed a series of relative valuation frameworks across edtech and education companies.

For each company, I:

Identified a relevant peer group

Mapped valuation (EV/EBITDA) against measures of financial performance

Evaluated how tightly valuation clusters around those performance metrics

The objective:

Does financial performance still explain valuation dispersion across stocks?

My conclusion:

AI has clearly influenced sector valuation multiples.

But at the company level the underlying valuation framework remains surprisingly intact.

Across the names analyzed, differences in valuation are still largely explained by revenue growth. For Coursera, revenue and profitability.

AI may be shifting the level of valuations, but it is not redefining the rules by which companies are valued relative to one another.

In this piece I focus on the following companies:

Coursera: COUR

Duolingo: DUOL

Stride: LRN

Postsecondary stocks: STRA; PRDO; UTI; APEI, CVSA; LOPE; LINC; PXED

As with any relative valuation exercise, results are inherently sensitive to peer group construction. Including or excluding companies can impact the explanatory power of the regression.

The peer sets are designed to reflect similar business models, comparable scaling dynamics, and analogous end markets. The goal here is not precision though. We are working with inherently imperfect comparables.

To avoid the temptation of creating peer groups for the expressed purpose of supporting the conclusions I want to create, I initially used ChatGPT to generate peer sets and then applied judgment to exclude companies that deviated too far from the target company’s operating model.

Coursera Valuation: Trading in Line with Marketplace and Consumer Stocks

Coursera is best understood as a marketplace business with a subscription revenue model. It connects learners, institutions, and enterprises, facilitating the distribution of content at scale. The underlying economics are consistent with other marketplaces: aggregation of demand and supply; operating leverage as volume grows; network effects.

The stock has fallen by half since last summer. In December management announced a merger with its competitor Udemy. At the time I expected the transaction to act as a catalyst for stock price appreciation. My rationale: increased scale with $115M of identified run-rate cost synergies would meaningfully improve profitability; the acquisition would give the new company at least a year to fix Udemy’s business model. On the stock price performance, I was wrong.

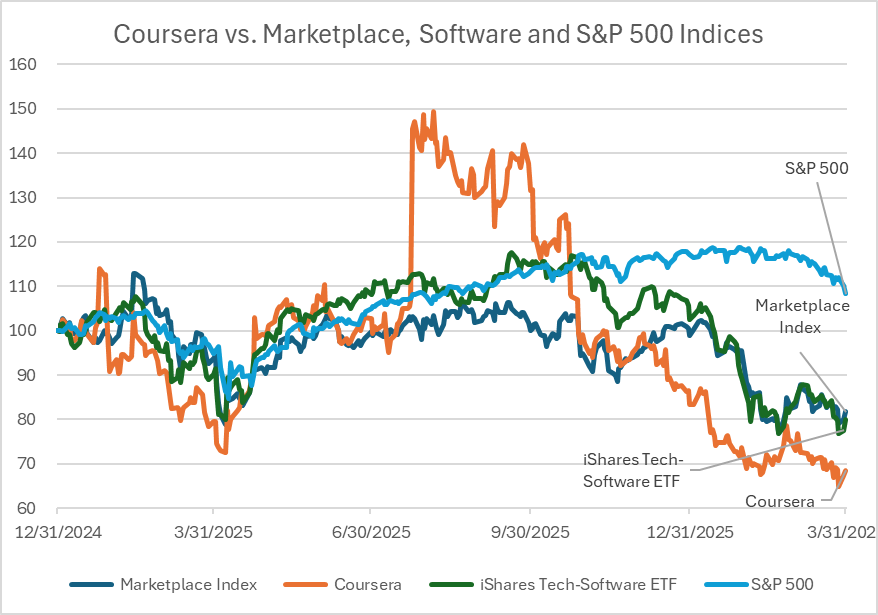

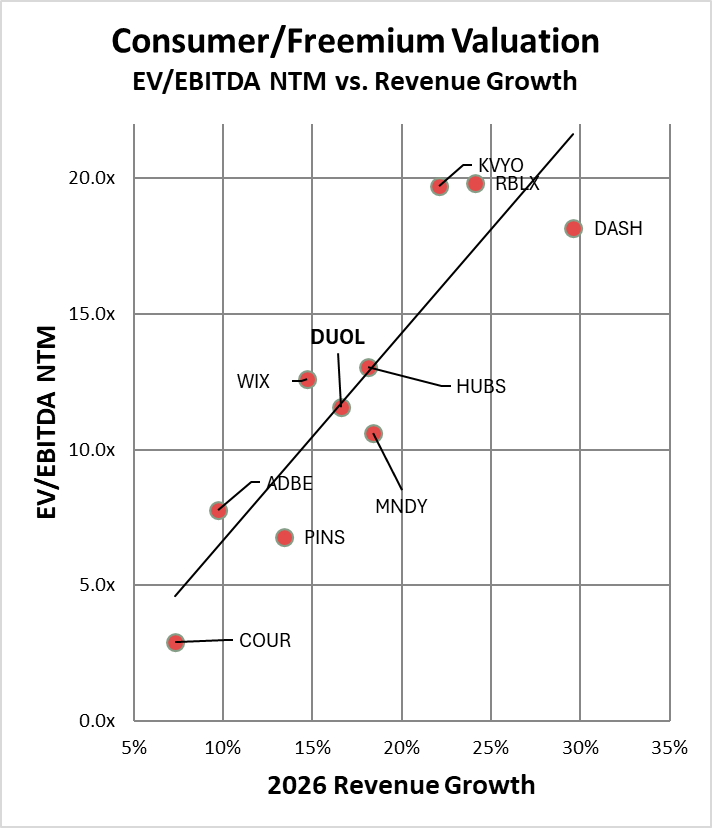

To evaluate Coursera’s valuation, I compare it against a group of consumer and marketplace businesses, including Roblox, DoorDash, Pinterest, HubSpot, Wix, Adobe, monday.com, Klaviyo, and Duolingo.

Yes, these companies operate in different end markets like gaming, food delivery, content, etc… But they share similar characteristics: demand aggregation, user engagement, monetization layers, and operating leverage.

Roblox, for example, may be a game that your kid plays, but it monetizes user-generated content and transactions. DoorDash and Uber are more traditional marketplaces. Wix and HubSpot layer monetization on top of a large base of users.

Since the start of 2025, Coursera’s stock has lagged my constructed marketplace index, the S&P 500, and software benchmarks such as the iShares Expanded Tech-Software ETF.

This underperformance primarily reflects multiple compression. The company consistently exceeded quarterly consensus estimates.

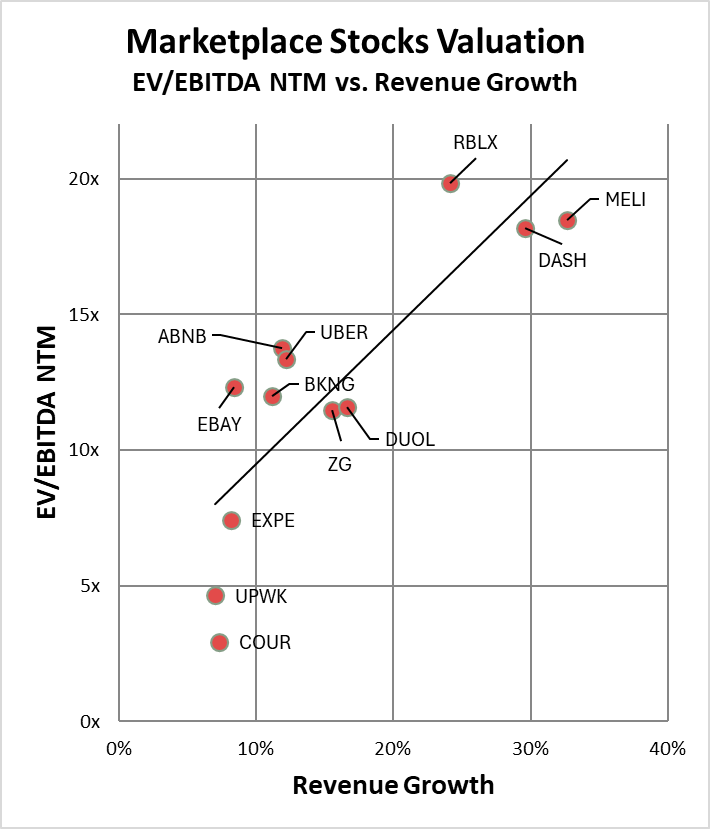

Regarding valuation, in the past investors were forced to value the stock on a EV/Revenue basis because the company didn’t generate profits.

Following the SaaSpocalypse, there has been an investor shift toward profitability, making EV/EBITDA the more relevant valuation metric.

Using this framework, the peer group shows a reasonably strong relationship between EV/EBITDA and revenue growth, with an R² of approximately 0.69.

As a reminder, a R² is the coefficient of determination, it measures how well a regression model can explain variation in data.

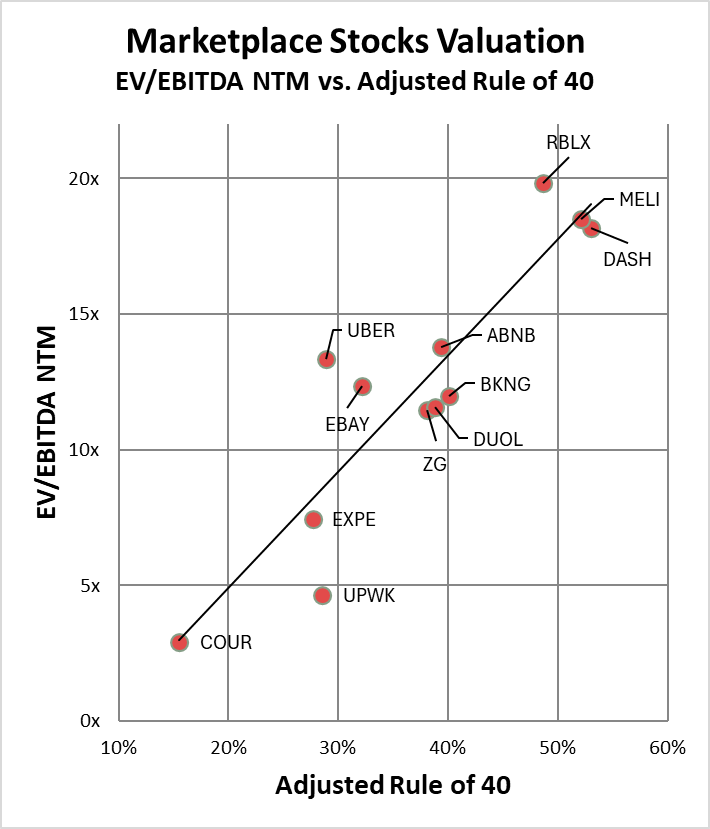

I also constructed a regression using an adjusted Rule of 40, which combines revenue growth and profitability into a single metric. The Rule of 40 is adjusted to weight revenue growth more than profitability.

When EV/EBITDA is plotted against the adjusted Rule of 40 of this comp group, the relationship strengthens meaningfully, with an R² of 0.82. Valuation across this group is better explained by the combination of growth and profitability than by growth alone.

In both frameworks, Coursera sits at the lower end of both regressions.

Its valuation aligns with its current growth and margin profile (as a standalone company).

In other words: the stock is trading where the model would suggest it should.

Well, not exactly… the current consensus estimates reflect the standalone business and do not incorporate the potential impact of the Udemy acquisition. $115M in expected cost synergies should improve EBITDA margins. Revenue by definition will improve optically because the combined company will be viewed relative to standalone Coursera revenue. I have no idea on a pro forma basis how the combined company will look, but stock screens don’t provide info to investment analysts on a pro forma basis.

If the combined entity delivers higher revenue growth and improved margins, the implication within this relative valuation construct is that a higher adjusted Rule of 40 should support a higher multiple.

Let’s just hope that Coursera and Udemy shareholders approve this merger in April and get the ball rolling. The stock could potentially move following management providing post-merger revenue and EBITDA guidance.

Duolingo: Trading In-Line with Consumer and Freemium Oriented Peers

Duolingo is a freemium, gamified language-learning app. Yes, it doesn’t have a clean comp set. That makes it difficult to value on a purely relative basis.

That said, the company shares characteristics with a range of publicly traded platforms:

Global scale with broad user reach

High-frequency engagement

A free-to-paid conversion funnel

Operating leverage

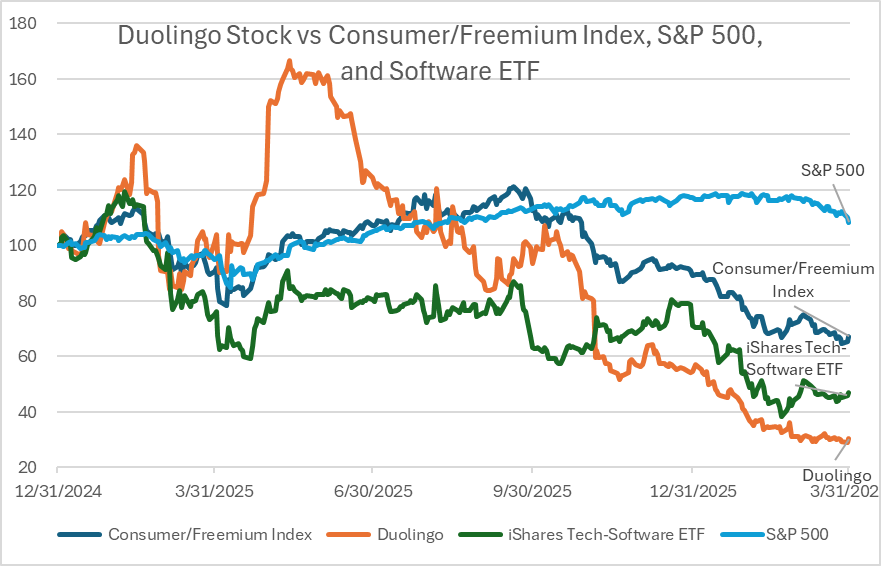

To benchmark valuation, I constructed a peer group that includes Roblox, DoorDash, Pinterest, HubSpot, Wix, Adobe, monday.com, Coursera, and Klaviyo. These companies operate in different verticals but again, they share common economic structures. The businesses are driven by usage, conversion, and retention.

Like Coursera, Duolingo has underperformed relative to its peer group. Since the start of 2025, the stock has lagged a broader consumer/freemium index, the S&P 500, and software benchmarks such as the iShares Expanded Tech-Software ETF. The stock saw meaningful stock price appreciation in mid-2025, but has since given back those gains, reflecting both multiple compression and concerns regarding the durability of its business model in an AI world.

Unlike Coursera, Duolingo’s valuation aligns with the traditional relationship between EV/EBITDA and revenue growth. Not adjusted Rule of 40 like Coursera.

When EV/EBITDA is plotted against revenue growth, the relationship is strong, with an R² of 0.81. In contrast, when valuation is plotted against an adjusted Rule of 40, the fit weakens materially, with R² declining to 0.50.

Within this peer set, Duolingo does not show up at the high end of either growth or valuation. Rather, it sits in the middle of the group, with a multiple that is broadly consistent with its current financial profile. If you take a look at the chart, it actually sits on the regression line. Meaning that at the current level on a relative basis the stock is neither a screaming buy nor a short.

Stride - K-12 Operator Valued Within a Postsecondary Framework

Stride is primarily a K-12 education company whose operating model is driven by virtual school enrollment and funding levels. It is the only pure-play publicly traded K-12-focused operator, with no direct peer set. While Pearson owns a competing asset (the division formerly known as Connections Education, my professional alma mater), its broader mix of businesses makes it an imperfect comp for valuation purposes.

There is no clean comp for this company. To the consternation of its investor base.

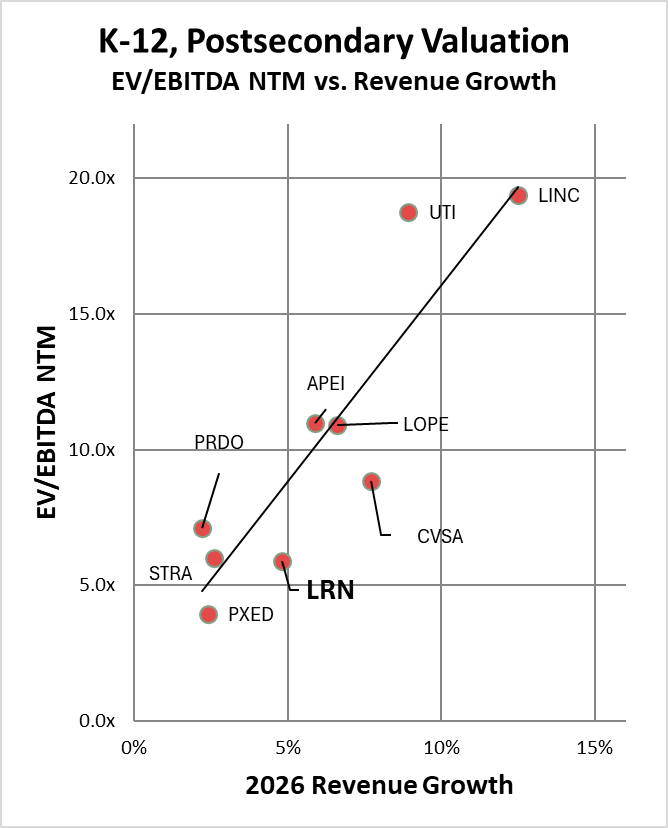

Despite being an orphaned stock, my sense is that investors for better or worse anchor the company within the broader peer group of publicly traded postsecondary education operators like Strategic Education, Perdoceo, Universal Technical Institute, and Lincoln Educational Services. Those operators are valued primarily through a relationship between revenue growth and EV/EBITDA multiples.

The postsecondary peer group exhibits a strong relationship between growth and valuation, with an R² of 0.82. Including Stride in the regression reduces the R² modestly to 0.80, suggesting that while it is not a perfect fit, it still aligns reasonably well within the same valuation framework.

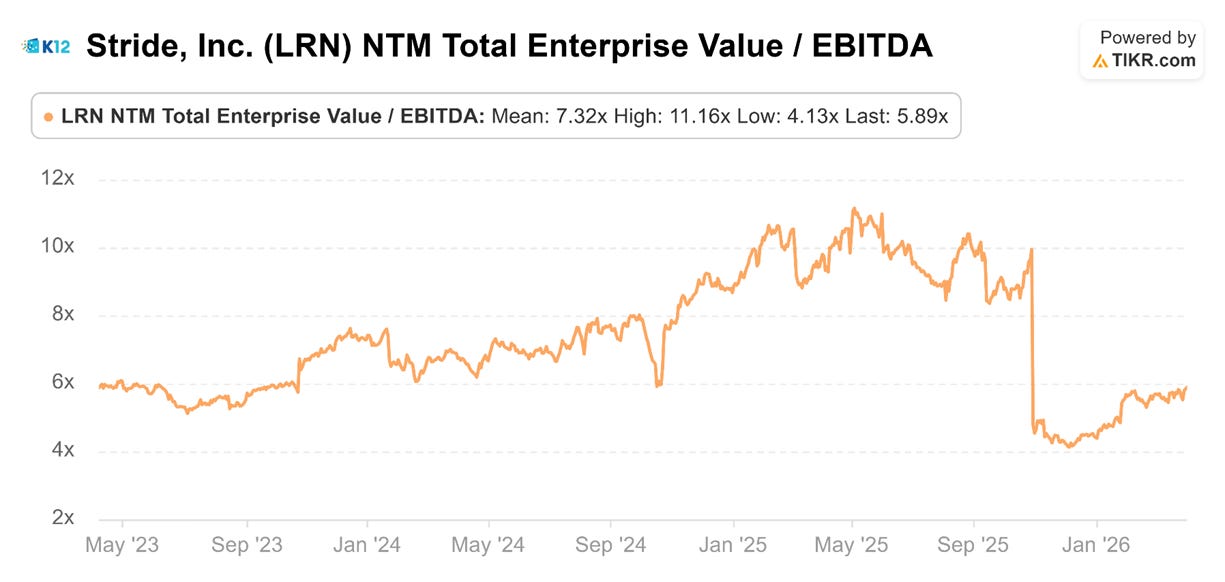

Historically, Stride traded at 5-6x EV/EBITDA. During the pandemic, enrollment tailwinds drove stronger revenue growth which in turn increased revenue and profitability. Interestingly, as you can see from the chart below what drove multiple expansion began in earnest in fall of 2023. Perhaps with the realization that the virtual school proposition was a secular growth story rather than a temporary cyclical Pandemic benefit. At its peak over the summer of 2025, the stock traded closer to 10x EV/EBITDA.

More recently, the stock declined by over 50%, driven in part by operational challenges related to a transition to a new learning management system. When the company reported earnings in January, the stock price increased over 20% as investors saw that the tech issues had stabilized.

When viewed through the regression of EV/EBITDA against revenue growth for the broader postsecondary peer group, Stride appears undervalued on a relative basis. Based on the company’s current growth rate, the implied multiple is closer to ~8.5x EV/EBITDA compared to its recent trading levels nearer to ~6x.

If Stride posts a good Q3 print, this valuation framework potentially implies that the valuation multiple will expand up to where the regression suggests it belongs.

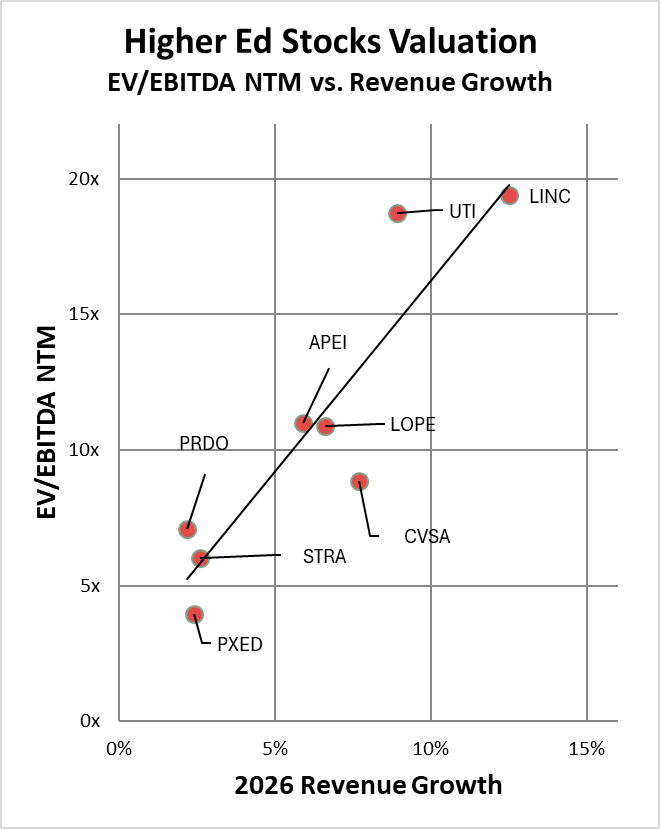

Postsecondary: Valuation Anchored to Revenue Growth

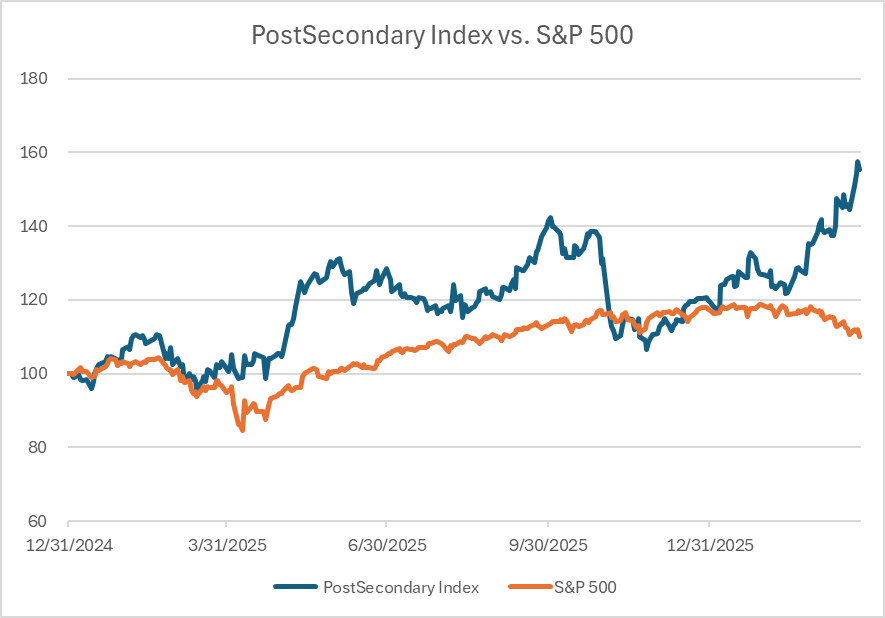

In Q1 2026, the postsecondary group materially outperformed the S&P 500, delivering high double-digit returns versus a roughly -7% decline in the broader market. This divergence suggests a sector-specific re-rating, rather than a macro-driven move.

That performance, however, was highly concentrated. A small number of names—most notably Lincoln Educational Services (+69%), American Public Education (+51%), and Universal Technical Institute (+42%)—accounted for the majority of the gains.

The best model to explain the sector’s relative valuation is the relationship between revenue growth and EV/EBITDA. The key drivers—enrollment trends, pricing, and program mix—flow directly into revenue growth, which in turn drives valuation multiples.

Higher-growth institutions command higher EV/EBITDA multiples. Lower-growth operators trade at a discount.

What’s more notable is how tightly these companies cluster around a regression line.

Three distinct groupings emerge:

Vocational / campus-based operators (UTI, LINC) sit at the high end—both in terms of growth and valuation. These businesses appear to benefit from strong demand and clearer alignment with workforce outcomes. Their underlying professions may also be less susceptible to near-term AI disruption (e.g., skilled trades).

Nursing and ground-campus exposure (APEI, LOPE, CVSA) cluster in the middle. They combine moderate growth with mid-tier valuation multiples. AI won’t replace nurses.

Online-heavy models (STRA, PRDO, PXED) screen at the low end, with lower growth and correspondingly lower valuation multiples. These models may face greater competitive pressure and potential substitution risk in certain white-collar pathways.

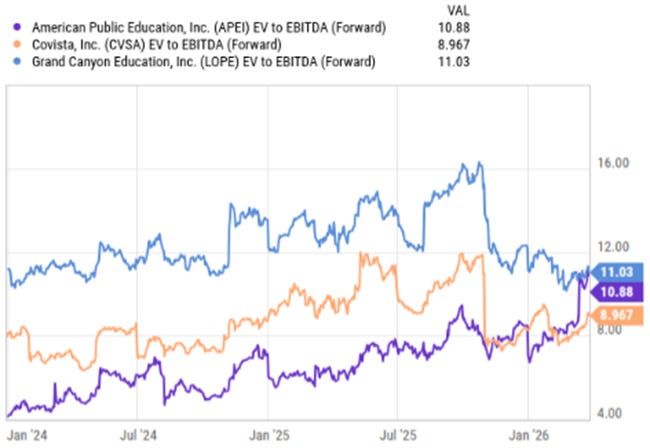

The divergence in valuation across postsecondary operators becomes even more evident when looking at multiple trends over time.

Vocational operators have seen the most pronounced re-rating. Both LINC and UTI have experienced sustained multiple expansion over the past 12–18 months, with forward EV/EBITDA multiples now at or near cycle highs. This reflects a combination of accelerating growth, improved execution, and investor preference for workforce-aligned education models.

In contrast, nursing and ground-campus institutions—including American Public Education (APEI), Grand Canyon Education (LOPE), and Covista (CVSA)—have exhibited more stable valuation trends. Multiples have generally moved within a narrower range, consistent with moderate but steady growth profiles and less volatility in underlying demand.

The most notable divergence is in online-focused operators. Strategic Education (STRA), Perdoceo (PRDO), and Phoenix Education Partners (PXED) have seen flat to declining multiples over the same period, with valuations remaining closer to cycle lows. These businesses have not benefited from the same multiple expansion, reflecting slower growth and increased skepticism around long-term positioning.

The data highlights the widening spread in valuation across programs. Vocational operators are being re-rated upward, while online models remain compressed, reinforcing a clear barbell in investor preference.

Conclusion

Despite the narrative around AI, the market is still valuing education and edtech companies using familiar frameworks.

At the individual company level, valuation remains grounded in financial performance. Revenue growth and profitability still explain where stocks trade. AI may be shifting the level of valuation multiples, but not the underlying relationship between growth and valuation.

Companies are still being rewarded based on what they actually deliver.

So for operators reading this piece, at least you know that the market isn’t acting totally irrational, and that you do have some say in how your company is trading in a post-AI world.

Disclaimer

This analysis reflects my personal views and is provided for informational purposes only. It should not be construed as investment advice or a recommendation to buy or sell any securities. The information presented is based on publicly available data and my own analysis, and while I believe it to be reliable, I make no representation as to its accuracy or completeness.

Investing in public equities involves risk, including the potential loss of principal. Readers should conduct their own due diligence and consult with a financial advisor before making any investment decisions.

I currently hold positions in Coursera (COUR), Udemy (UDMY), Stride (LRN), Phoenix Education Partners (PXED), and Strategic Education (STRA). My views may change at any time without notice.

This analysis was created with the assistance of AI for editing and visualizations.