Chegg’s Third Act: Do Value Investors Have It Right?

An activist investor sees meaningful upside in Chegg (CHGG). We examine whether Busuu, Chegg Skills, and the company’s balance sheet/cash flow justify that optimism.

Back in April, several subscribers asked for my thoughts on edtech provider Chegg after Galloway Capital Partners disclosed a 5.44% beneficial ownership position in the company and publicly commented that the company was undervalued.

Galloway Capital Partners issued a press release with a quote from Chief Investment Officer Bruce Galloway stating that

We believe Chegg is materially undervalued and that the current share price reflects a fundamental misunderstanding of the business… with a more focused strategic structure and continued execution, we see a clear and actionable path to unlocking significant shareholder value.

The stock subsequently approached $1.50, nearly doubling from its April lows. I promised my subscribers I would take a closer look if the shares fell back below $1, which seemed likely once the initial excitement surrounding the activist investment subsided.

That has now happened.

Chegg recently traded at $0.85 per share, representing a market capitalization of roughly $96M.

Readers who didn’t ask for this analysis may reasonably wonder why they should care about a $100M microcap stock. There are far larger companies generating more consequential investment debates. For example, investors are still trying to determine whether Microsoft and the other hyperscalers that collectively are worth trillions of dollars will earn adequate returns on their enormous AI infrastructure investments.

So, what’s so interesting about Chegg?

Chegg is a case study in how investors should assess a deeply disrupted company that may still own valuable assets.

More than half of Chegg’s shareholder base appears to consist of retail investors (Yahoo Finance says that institutions own 40%). It seems like the discourse on social media is punching above its weight class.

Most investment narratives ultimately reduce to a relatively simple question.

For Chegg, that question is:

What’s Busuu worth?

Chegg acquired the language-learning platform for $436M in 2021. If Busuu were still worth anything close to that purchase price, Chegg’s stock would have substantial upside.

A lot has changed since 2021. That year represented a period of peak edtech valuations, fueled by post-pandemic enthusiasm for virtual and digital learning.

At two times 2025 revenue, Busuu could be worth as much as Chegg’s entire current market capitalization. At three times revenue, the value of Busuu alone could materially exceed it.

Galloway’s involvement introduces a second question:

Can an activist investor cause that value to be recognized through better disclosure, restructuring, asset sales, or other strategic action?

I somewhat agree with Galloway’s assertion regarding unlocking shareholder value. If management were to sell Chegg’s assets tomorrow to strategic buyers, the value of the company may exceed the current market capitalization.

The complicating factor though is that a near-term transaction involving all or part of Chegg seems unlikely.

Chegg hired Goldman Sachs in 2025 to examine strategic alternatives, but the board ultimately decided to remain independent. Management is now overseeing the measured decline of Chegg Study while attempting to build a new enterprise-skilling business around Busuu and Chegg Skills.

That process will take time, and its duration will depend partly on how quickly Chegg Study continues to decline and how rapidly management can remove costs. Chegg’s legacy Academic Services business generated roughly $308M of revenue in 2025, down approximately 43% YoY. The rapid decline of Academic Services likely complicates any transaction, because a buyer would need to assess the durability of its cash flow and the remaining costs required to operate and restructure the business. It may take more than a year for Chegg Study to at minimum reach a smaller and more stable operating base, assuming that product isn’t sunset altogether.

As an edtech practitioner, I see a legitimate opportunity for Chegg to use generative AI to lower content-development costs, increase its catalog, and compete in enterprise learning. Chegg can establish itself as a disruptor that meaningfully offers a lower price point than larger rivals. Whether lower content-development costs are enough to overcome weaker distribution remains unproven.

Assuming that a transaction doesn’t take place anytime soon, I can make a reasonable argument that the company trades between $0.50 and $1.50 per share.

Given that, regarding my own portfolio I might start a position at the lower end of the range. In my estimation this would provide a comfortable margin of safety, taking into account the value of Busuu, cash on hand, and optionality of an activist investor like Galloway.

Regarding Galloway overall, Galloway deserves credit for bringing attention to the gap between Chegg’s current market value and the potential value of its underlying assets. Its activism potentially could provide shareholders a service if Galloway pushes for better disclosure and a disciplined approach to realizing value from Busuu and Chegg Skills. It’s a good thing in general for an engaged shareholder to ask difficult questions to a management team.

Chegg’s Three Acts and Two Reinventions

Chegg is entering its third act and attempting its second major reinvention.

In its first act, Chegg built a recognizable student brand by allowing college students to rent expensive textbooks. It went public with this business model, whose obvious flaw was the inevitable shift from physical textbooks to digital course materials.

Chegg’s second act was far more successful, for a time. Under current CEO Dan Rosensweig, the company created a digital subscription platform centered on Chegg Study. Chegg provided students “homework help” in the form of textbook solutions and expert answers.

Chegg became a high-margin digital subscription business, generated substantial cash flow and, at its peak, achieved a market capitalization in excess of $10B. That cash flow also allowed Chegg to acquire businesses intended to expand the company beyond its core academic-services offering.

Generative AI brought the second act to an abrupt end.

Students could obtain immediate answers and explanations from ChatGPT, Google, and other AI tools. Chegg Study’s historical content advantage became significantly less valuable.

Chegg’s third act is focused on corporate customers.

The company is taking assets that previously served individual consumers and repositioning them to sell language and workforce training to employers, institutions, and distribution partners.

That transformation centers on two businesses:

Busuu, the company’s language-learning platform.

Chegg Skills, its workforce-training and reskilling business.

Together, Chegg reports them as Chegg Skilling.

Is Chegg Below Its “Intrinsic Value”?

Galloway argued that Chegg’s stock trades at a substantial discount to intrinsic value.

I don’t necessarily disagree with their assertion, but I would frame the opportunity slightly differently.

I would say that Chegg trades below the potential value of its assets.

That isn’t quite the same thing as intrinsic value.

Intrinsic value ultimately depends on the cash a business can generate for shareholders, together with the value of its net assets. Chegg doesn’t disclose enough information to determine how much sustainable cash either business (Busuu or Chegg Skills) currently produces or will produce in the future.

Chegg effectively owns three components:

A declining legacy academic-services business that should continue generating cash as it contracts.

Busuu

Chegg Skills

For the legacy business, the key question is whether the remaining cash generated by Chegg Study exceeds the maintenance, restructuring, and eventual shutdown costs associated with it.

If the answer is yes, the legacy business could help finance Chegg’s transformation.

If the answer is no, it could consume part of the value that might otherwise belong to Busuu and Chegg Skills.

Chegg previously expected Busuu to reach adjusted EBITDA profitability by Q1 2026, while describing Chegg Skills as being on a path toward profitability. Chegg Skilling revenue grew 9% year over year in the first quarter of 2026, and management expects double-digit growth for the full year.

That’s encouraging, but it doesn’t necessarily mean the businesses will produce substantial cash flow in 2026.

There’s also a great deal investors don’t know about Chegg Skilling, which makes its future cash generation difficult to assess.

Standalone Busuu and Chegg Skills revenue.

B2C versus B2B revenue.

Enterprise bookings, customers, and average contract values.

Renewal and retention rates.

Gross margins and adjusted EBITDA.

The Market Is Assigning Close to $60M to the Operating Businesses

As of Q1 2026, Chegg had close to $68M in cash and $34M of convertible debt, leaving net cash of roughly $34M, or close to $0.30 per share.

At a share price of $0.85, investors are therefore paying approximately $0.55 per share for the operating businesses.

With close to 112M shares outstanding:

$0.55 per share × 112M shares = $62M

That $62M represents the market’s implied value for:

Busuu

Chegg Skills

The remaining cash flow from Chegg Study

Less corporate overhead

Less future restructuring and shutdown costs

Less the investment required to complete the B2B transformation

Chegg Skilling generated $17.6M of revenue in the first quarter of 2026. Annualized, that equals a revenue run rate of roughly $70M.

If we attribute the full $62M operating value to Chegg Skilling (and assume no value either positively or negatively for the legacy business), the market is valuing the segment at:

$62M ÷ $70M = 0.9× annualized revenue

Other publicly traded edtech companies trade at similar revenue multiples. Coursera, for example, trades near 0.6× EV/revenue. Skillsoft (SKIL) trades at 1x EV/Sales.

Look, I own Coursera and believe it’s substantially undervalued. The company is being penalized by a narrative that AI may substitute for traditional online learning.

But on a relative basis it’s difficult to argue that Chegg is somehow meaningfully mispriced.

On an absolute basis, the key question is what a strategic buyer might eventually pay for Chegg’s assets.

In my opinion, we’re unlikely to know that answer soon.

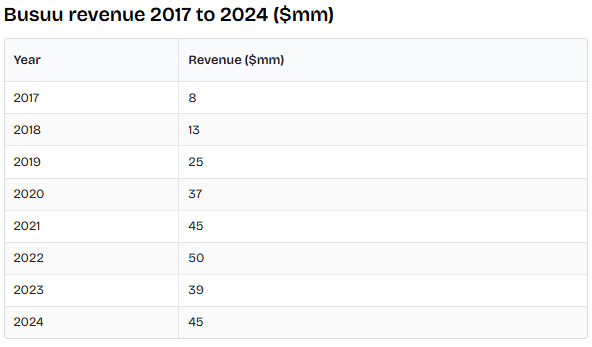

Busuu’s Post-Acquisition Performance Was Disappointing

Chegg acquired Busuu in 2021 for $436M. At the time, Busuu generated roughly $45M in revenue and was growing by more than 20% annually.

Several years later, revenue remains roughly comparable to where it was when Chegg acquired the company.

Chegg acknowledged in its Q3 2023 earnings call that the execution and integration of Busuu had not gone as planned. Third-party estimates suggest Busuu’s revenue may have declined in 2023 to $39M, an especially disappointing result for an asset purchased at a substantial revenue multiple.

More recent performance appears better.

Management reported that Busuu revenue YoY grew:

9% in 2024.

7% in Q1 2025.

15% in Q2 2025.

Chegg also indicated that Busuu was on track to generate approximately $48M of revenue in 2025.

Growth appears to be driven primarily by enterprise customers.

In Q2 2025, Chegg reported that:

Busuu’s B2C revenue grew 6%.

Busuu’s B2B revenue grew 39%.

Total Busuu revenue grew 15%.

Those figures suggest that B2C still represented most of Busuu’s revenue.

If B2B had already been the larger business, Busuu’s overall growth rate would have been much closer to 39%. Instead, total revenue grew 15%, much closer to the 6% growth reported by the consumer business.

Based on the reported growth rates, I estimate that B2B represented roughly one-third of Busuu’s Q2 2025 revenue, with B2C accounting for approximately two-thirds. Again, that’s only an estimate. I also have no idea what this revenue split might look like in 2026.

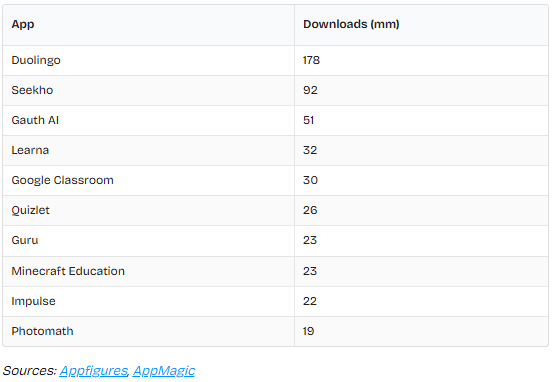

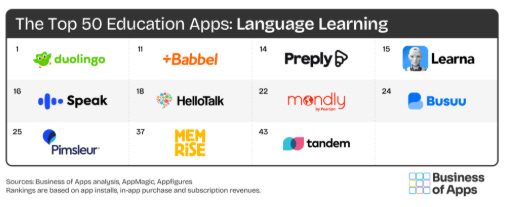

The thing to remember is that Busuu isn’t the category leader in language learning, that position belongs to Duolingo.

Duolingo isn’t just the premier global language-learning application. It’s arguably the dominant consumer brand in edtech and the most widely downloaded education app in the world.

Duolingo generated roughly $250M of revenue in 2021 and has since approached $1B. Busuu, by comparison, remains near $50M of annual revenue during that time.

Most Popular Education Apps 2025

In a Business of Apps ranking of education applications, Busuu ranked 24th. Rankings are based on installs, usage, and in-app revenue.

Jack Welch (the former CEO of General Electric for you Gen Z readers) used to say that his business units needed to be number 1 or 2 in their industry or be sold.

So it’s a bit unnerving to create an investment thesis based on a 24th ranked app. Yes, I realize that the focus is on enterprise rather than consumer. But a fair amount of revenue is still consumer.

It’s conceivable that Busuu can maintain its consumer base while executing its enterprise strategy. It’s also possible that the opposite is true, that competition could erode the consumer revenue base.

Color from Chegg management on conference calls would be helpful regarding Busuu and its market position.

What’s Busuu Worth?

Busuu could plausibly be worth between $50M and $150M today, in my opinion.

That range represents one to three times revenue, assuming annual revenue near $50M.

A valuation toward the higher end could be justified if Busuu demonstrates:

Sustained double-digit growth

Continued enterprise penetration

Strong customer retention

Positive adjusted EBITDA

Declining dependence on consumer revenue

Resilience from AI substitution by LLMs

A valuation near the low end would be more appropriate if:

Consumer growth stalls or declines

Enterprise growth falls below double digits

The business remains unprofitable

Customer retention is weak

Duolingo recently traded at approximately 3.8× enterprise value to sales and roughly 15× enterprise value to EBITDA. Applying a similar sales multiple to Busuu would imply a value approaching $185M.

But Busuu isn’t Duolingo. It isn’t the dominant edtech app. It doesn’t have Duolingo’s revenue growth and margin characteristics.

A strategic buyer might nevertheless value Busuu more highly than public investors currently do inside Chegg.

A larger language-learning or education company might be able to:

Eliminate duplicative corporate expenses.

Combine marketing spending.

Cross-sell Busuu into an existing customer base.

Integrate Busuu with a broader product suite.

Accelerate enterprise distribution.

Chegg Skills Is a Small Player in a Fragmented Market

Chegg acquired Thinkful for roughly $80M in 2019. Thinkful originally operated as a direct-to-consumer coding bootcamp. Chegg has since repositioned the business as an employer- and partner-distributed workforce-training platform.

Chegg Skills may have generated $20M to $25M of revenue in 2025. That is only an estimate because Chegg does not report its Chegg Skilling businesses separately.

Learners generally access these programs through employers, edtech corporate intermediary Guild or other distribution partners. Note that there are a plethora of bootcamp type companies, some of whom are larger than Chegg Skills. These include General Assembly (perhaps the largest operator), Flatiron, Galvanize and others.

From a valuation perspective, Coursera is the closest publicly traded reference point, although the business models aren’t directly comparable. Chegg Skills is closer to an employer-funded online bootcamp than to an education marketplace like Coursera/Udemy.

Coursera aggregates courses, certificates and degrees from universities and major technology companies. It serves consumers, businesses, universities and governments.

Chegg Skills offers a narrower set of more structured, career-oriented programs, often involving projects, coaching and learner support.

The biggest challenge I see with scaling Chegg Skills is distribution.

Generative AI could allow Chegg to build a much broader self-service catalog at relatively low incremental cost. Chegg could potentially produce hundreds or even thousands of courses without requiring the enormous content investment that would have been necessary several years ago.

But presently, it lacks the distribution scale of Coursera or LinkedIn Learning.

There are other elements that Chegg Skills needs, like enterprise integration, skills verification, trusted credentials, etc… Investors have little sense as to where Chegg Skills sits competitively with its peers and the level of investment required to scale.

What Are Busuu and Chegg Skills Worth Together?

Using broad valuation ranges:

Busuu could be worth approximately $50M to $150M.

Chegg Skills could be worth approximately $10M to $25M.

That implies a combined value of roughly $60M to $175M.

At the high end, the assets could be worth substantially more than Chegg’s current enterprise value.

At the low end, they may be worth the value the market already assigns to the stock.

It isn’t difficult to see why Galloway then is taking an activist stance in this stock.

What An Activist Investor Can Do

An activist investor can push Chegg to pursue several actions that may improve the value of Busuu and Chegg Skills.

Improve Disclosure

This is the most immediate and least risky opportunity.

Chegg could separately report:

Busuu revenue and growth

Chegg Skills revenue and growth

B2C and B2B revenue

Enterprise bookings

Annual recurring revenue

Customer counts

Average contract values

Renewal rates

Gross margins

Adjusted EBITDA

Cash flow

If the businesses are performing well, improved transparency could materially improve the stock’s valuation without requiring a transaction.

Currently investors don’t know enough about these two assets to know what they are really buying.

It’s not enough to say that Busuu is worth 2 or 3x revenue. Investors to assign a higher multiple need to know exactly why Busuu is so valuable. Assuming favorable trends, increased disclosure can absolutely help.

Consolidate the Edtech Enterprise Market

A more ambitious albeit riskier strategy would use Busuu and Chegg Skills as the foundation for a broader enterprise-training platform.

The workforce-learning market remains highly fragmented. Numerous specialized providers generate less than $50M of revenue.

The strategic logic would be to acquire other vendors that have not scaled and cross-sell into enterprise customers.

Chegg would need to acquire businesses inexpensively, integrate them effectively, and demonstrate real cross-selling.

On paper this may sound like a good idea. The reality is that this is really hard to do.

Sell Busuu and Chegg Skills, Perhaps in a Year or Two

The obvious way to create value is to sell Busuu and Chegg Skills to the highest bidder.

Chegg to my knowledge hasn’t disclosed Goldman Sachs’s evaluation of strategic alternatives.

Chegg’s board ultimately decided to remain independent.

Possible explanations include that buyers:

Offered less than the board considered acceptable

Wanted to buy parts of the company rather than the whole, including the declining Chegg Study business

Questioned the quality or trajectory of the assets

Wanted more evidence of enterprise growth and profitability

I am assuming that given the situation with the legacy business Chegg likely had to attempt to sell the entire company rather than its individual components.

So my hypothesis is that once the company sunsets the legacy product, a sale becomes much more doable.

So, Do Value Investors Have It Right?

Perhaps, on paper.

Under an optimistic scenario, the combined assets could be worth substantially more than Chegg’s current market capitalization.

But we are dealing with a publicly traded company with illiquid assets under a strategy that may see challenged execution.

What can go wrong includes:

Chegg Study revenue declines faster than costs can be removed.

Restructuring and shutdown costs exceed expectations.

Busuu’s B2C revenue stalls or declines.

Busuu’s enterprise growth slows.

Enterprise sales cycles require more investment than expected.

Chegg Skills fails to gain meaningful distribution.

AI further commoditizes generic training content.

The assets can’t be sold at attractive valuations.

The stock remains illiquid and volatile without a near-term catalyst.

Conclusion

Management has assembled a credible strategy given the assets that they have.

CEO Dan Rosensweig previously led Chegg through a successful reinvention, which gives management some credibility. Whether that experience translates to a B2B enterprise-learning strategy remains an open question.

As an investor, I personally would want a larger margin of safety.

Here are the things that I’m going to focus on when the company reports its results:

level of degradation of the core business. This matters because the core business is supposed to provide cash flow to grow other parts of the business.

Overall cash flow that the company generates

Revenue growth of Chegg Skilling, whether it’s double digits or not.

A lot can go right, a lot can go wrong.

I’d become more interested if the stock declined another 30% to 40%, assuming the balance sheet and operating outlook remained broadly intact.

Disclaimer

I don’t currently own shares of Chegg. I own shares of Coursera.

This article reflects my personal opinions and is provided solely for informational and educational purposes. It isn’t investment advice or a recommendation to buy or sell any security. Investors should conduct their own research and consider their individual financial circumstances and risk tolerance before making an investment decision.